2024 Burial Insurance with Kidney Disease

last updated on January 31, 2024

last updated on January 31, 2024Some insurance companies offer first-day coverage insurance for kidney disease patients undergoing treatments or dialysis in recent years.

This article will provide information on qualifying for the best plan with the best rates.

FOR EASIER NAVIGATION:

- Can I Get Burial Insurance With Kidney Disease?

- Types Of Burial Insurance Available For Kidney Disease Patients

- What Is My Best Insurance Option If I Have Kidney Disease?

- How Much Does Burial Insurance Cost If I Have Kidney Disease?

- Do I Need A Medical Exam To Qualify For Burial Insurance?

- Burial Insurance Underwriting With Kidney Disease

- Information We Need If You Have Kidney Disease

- What If My Insurance Application Was Rejected Because of Kidney Disease?

- How To Get First-Day Coverage Insurance

- How Can Funeral Funds Help Me?

- Frequently Asked Questions

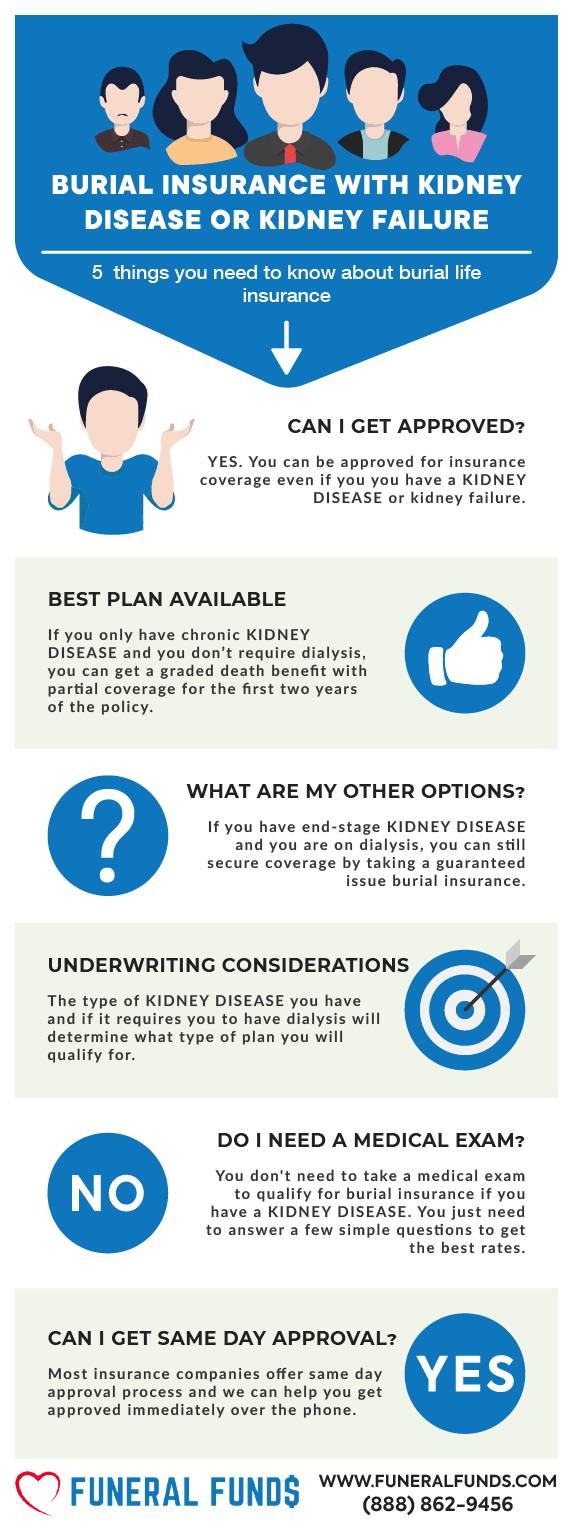

Can I Get Burial Insurance With Kidney Disease?

Yes, you may even qualify for first-day coverage, no waiting period insurance if you are compliant with taking treatments and medications for your kidney condition.

Types Of Burial Insurance Available For Kidney Disease Patients

First-Day Coverage – There’s no medical exam to qualify for this plan. You will only need to answer some basic health questions. The best feature of this plan is there is no waiting period. You are fully covered from your first payment, and your beneficiary will receive your 100% death benefit when you pass away.

Guaranteed Issue Whole Life Insurance – This is a no medical exam and no health questions policy. Guaranteed issue life insurance has a two-year waiting period for natural causes of death. If you die from an illness, the insurance company will pay your beneficiaries the refund of all your premiums plus 7-10% interest. After the two-year waiting period, your policy will pay a 100% death benefit if you die for any reason.

What Is My Best Insurance Option If I Have Kidney Disease?

Chronic Kidney Disease (Renal disease) – First-day coverage insurance is your best option if you have kidney disease and are not on dialysis. Some insurance companies offer first-day coverage depending on your residence (plans are not offered in all states).

Kidney disease with Dialysis – Your best insurance option if you have end-stage kidney disease or have kidney disease and receive dialysis is a first-day coverage insurance. However, you must be following a prescribed treatment plan from your doctor.

If your doctor prescribes dialysis treatment, and you refuse, your only option would be a guaranteed acceptance life insurance with a two-year waiting period.

Kidney Transplant – Your best option for insurance coverage is guaranteed issue life insurance, no medical exam, and no health question policy if you had a kidney transplant or your doctor recommends a kidney transplant. If your transplant occurred more than five years ago, you may also have a first-day coverage option, depending on what state you live in.

How Much Does Burial Insurance Cost If I Have Kidney Disease?

The cost of burial insurance if you have kidney disease will depend on your:

- Age

- Gender

- State of residence

- Smoking status

- Type of policy

- Coverage amount

Do I Need A Medical Exam To Qualify For Burial Insurance?

No, you don’t need to take a medical exam to qualify for burial insurance with kidney disease or kidney dialysis.

You only have to answer basic questions about your health. The application process is simple, and you don’t need to provide medical records or blood and urine samples. You’ll often get official approval from the insurance company within minutes!

Burial Insurance Underwriting With Kidney Disease

Every life insurance company with underwriting asks health questions and performs a prescription history check to determine your life insurance eligibility.

You will find these terms in the health questionnaire referring to kidney disease:

- Kidney disease

- Renal disease

- Chronic kidney disease

- Chronic renal disease

- End-stage kidney disease

- End-stage renal disease

- Kidney transplant

- Dialysis

Insurance companies will commonly ask kidney disease questions this way:

- Have you ever been diagnosed, treated for, or advised to have treatment for kidney disease?

- During the past 24 months, has the Proposed Insured been diagnosed by a physician as having or been treated for kidney disease (including dialysis) or chronic kidney disease?

- Have you ever been diagnosed with, received, or been advised to receive treatment or medication for kidney disease?

- In the past 10 years, have you opted not to seek treatment, have not taken medication, or have not followed the prescribed treatment plan following a medical diagnosis of kidney disease?

If you have any kidney disease, you must answer “yes” to the kidney disease question, however they phrase it.

PRESCRIPTION HISTORY CHECK

Here’s a list of common prescription medications for kidney disease:

- Amlodipine

- Atorvastatin

- Azathioprine

- Calcitriol

- Cinacalcet

- Cyclosporine

- Fosrenol

- Flomax

- Levocarnitine

- Mycophenolate

- Nifedipine

- Perindopril or Ramipril

- Phosex

- Prednisolone

- Renagel

- Sirolimus

- Tacrolimus

If you’re taking any of these meds, the insurance company will know you are receiving kidney disease treatments.

Information We Need If You Have Kidney Disease

To get you the best rates, here are some questions we may ask about your kidney disease:

- Are you taking medications for your kidney disease? What are they?

- Are you undergoing dialysis?

- Do you have any surgery to treat your kidney disease?

- Do you have other health conditions aside from kidney disease?

- Have you been hospitalized in the past 12 months because of kidney disease?

- Have you been recommended to receive a kidney transplant?

- What type of kidney disease do you have?

- When were you diagnosed with kidney disease?

Be sure to answer every question honestly. The more information you provide, the better your chances of finding affordable first-day coverage insurance.

What If My Insurance Application Was Rejected Because of Kidney Disease?

If your insurance application was rejected in the past because of kidney disease, we help clients get approved for this kind of life insurance by shopping multiple life insurance companies that accept applicants with kidney problems.

Kidney transplant patients can get a guaranteed acceptance life insurance plan with no medical exam or health questions where they will be approved regardless of their health.

How To Get First-Day Coverage Insurance

The best way to find first-day coverage burial insurance is to work with an independent life insurance agent who knows the best insurance companies that offer first-day coverage life insurance policies for people with kidney disease.

The life insurance experts at Funeral Funds of America guide their clients through the entire insurance application process.

How Can Funeral Funds Help Me?

You don’t have to waste time searching with multiple insurance companies because we can do this work for you. We work with many A+ rated insurance carriers specializing in covering high-risk clients.

Our licensed insurance agents search all the best companies to get you the best rates, and we promise to make the process quick and easy.

Fill out our quote form on this page or call us at (888) 862-9456, and we can give you an accurate quote.

Frequently Asked Questions

Is kidney disease a pre-existing condition for life insurance?

Yes, any health issue you have before the insurance application is considered a pre-existing condition in life insurance.

Can you get first-day coverage insurance if you have kidney disease?

Yes, you can get first-day coverage insurance with kidney disease, depending on your health and the state you live.

Can a person with kidney disease get burial insurance?

Yes, they can even qualify for a first-day coverage plan, depending on the state they live in and their overall health.

What are the benefits of having burial insurance if you have kidney disease?

Some benefits include peace of mind, financial security for your loved ones, and the ability to choose your burial arrangements.

Do I need to tell insurance about kidney disease?

You must disclose your kidney disease to the insurance carrier to get first-day coverage. Failure to do so could result in your policy being declined or canceled.

Is there an age limit for burial insurance for kidney disease?

You can apply for burial insurance if you are 18-89 years old.

What are the things that may affect my eligibility if I have kidney disease?

Your condition’s severity, current treatment plan, number of hospitalizations in the last two years, and any recommendations for a kidney transplant.

What is my best insurance option if I have chronic kidney disease?

A first-day coverage insurance is your best option if you have chronic kidney disease.

Can I qualify for cremation insurance with a history of kidney disease?

Yes, you may qualify for a first-day coverage.

Is there a waiting period for life insurance if you have kidney disease?

There is no waiting period if you qualify for a first-day coverage plan.

What is the maximum benefit amount for burial insurance if you have kidney disease?

Some policies offer up to $20,000 to $50,000 in coverage.

Can you be denied insurance for kidney disease?

You can be denied first-day coverage life insurance if you’ve been hospitalized two or more times in the last two years, if you are recommended to get an organ transplant, or if you’ve had a transplant in the last five years.

Can I get life insurance if I’m on kidney dialysis?

Yes, you may even qualify for a first-day coverage plan if you follow your doctor’s treatment plan and recommendation and live in the right state.

What happens if I have kidney disease and my life insurance policy lapses?

You will no longer have life insurance coverage. If you die without life insurance, your loved ones will be responsible for paying for your funeral and other end-of-life expenses.

What are some things to consider when choosing a burial policy with kidney disease?

Some things to consider include immediate coverage, the death benefit amount, and the type of policy you purchase.

Can I qualify for life insurance if I have end-stage kidney failure?

Yes, you may even qualify for a first-day coverage plan if you follow your treatment and doctor’s recommendations.

RELATED POSTS: