Life Insurance for HIV Positive [Use Caution]

last updated on January 16, 2025

last updated on January 16, 2025Getting life insurance for HIV positive is possible. However, your life insurance options are very limited.

IMPORTANT: Being HIV positive puts you in the high-risk category which will result in a mandatory two-year waiting period with every insurance company. No life insurance company will offer you a first-day coverage plan if you are HIV positive.

In this article, we will discuss what options you have when you have been diagnosed with HIV. In addition, we will teach you how to find affordable burial insurance with HIV.

| TABLE OF CONTENTS | |

|---|---|

What Is My Best Insurance Option If I Have A History Of HIV?

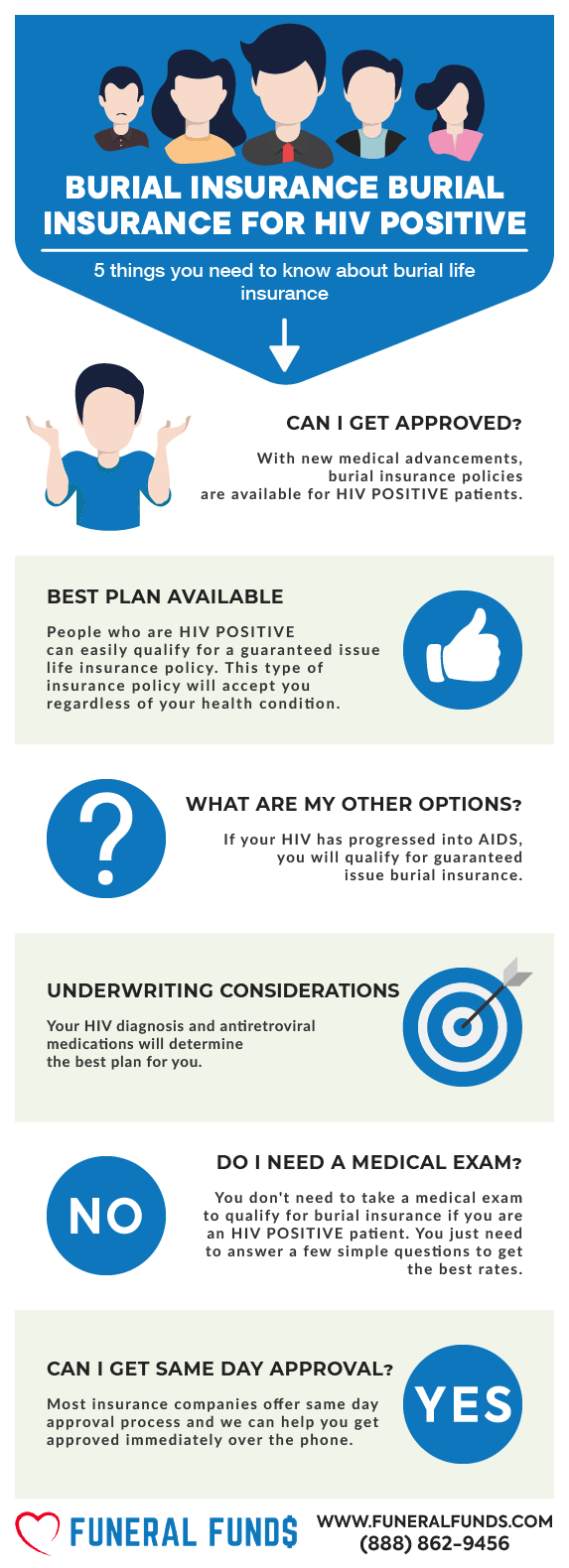

People with HIV can easily qualify for a guaranteed issue life insurance policy or automatic approval life insurance. This type of insurance policy does not require a medical exam or asking any health questions. Acceptance is guaranteed regardless of health condition.

Guaranteed acceptance life insurance is a small whole life insurance policy for covering final expenses and burial costs. Most plans are designed for people ages 50-85 years old.

Best Option: Guaranteed issue life insurance

WHAT ARE THE REQUIREMENTS TO QUALIFY FOR GUARANTEED ISSUE LIFE INSURANCE?

Only three requirements must be met before an applicant can qualify.

- The applicant must be a US citizen

- The product must be available in your state.

- The applicant must be between the ages of 50-85.

PROS OF GUARANTEED ISSUE LIFE INSURANCE

- Guaranteed acceptance life insurance policies require no medical exams, so people with poor health, like dialysis patients, can receive coverage automatically. Since there is no medical underwriting, application approval will only take days, not weeks.

- Guaranteed life insurance, like traditional term life insurance, pays cash to a beneficiary upon the insured’s death.

- You cannot be turned down even if you have a pre-existing condition. You’ll qualify for this policy as long as you are a US citizen and you meet the age requirement of 40-85.

- Small face amount options. Most guaranteed issue policies allow you to buy as low as $5,000 in coverage. You can only buy the amount that you need. You can do so to ensure your final expenses are taken care of.

CONS OF GUARANTEED ISSUE LIFE INSURANCE

- Guaranteed acceptance life insurance policies are usually limited to $25,000 in coverage. While it’s possible to buy multiple policies to make the total coverage exceed the $25,000 in coverage, it’s not a great option to consider financially.

- Most guaranteed acceptance life insurance policies cost more than traditional term or whole life insurance policies that require a medical exam. The cost of the premium is higher because insurance companies take on higher risk with this type of policy; they must charge more to cover their increased risk.

- Waiting period – All guaranteed issue life insurance policies have a graded benefit clause which states guaranteed life insurance policy will not provide coverage for natural causes of death for a specified period, typically two years once you purchase your life insurance policy.

A two-year waiting period before your guaranteed acceptance life insurance policy will provide coverage for natural causes of death.

DEATH BY NATURAL CAUSES

It is essential to understand what death by natural cause is. A natural cause of death is any type of death that is caused by an illness. An illness such as heart disease, cancer, stroke, diabetes, etc.

If an insured dies due to natural causes during the waiting period, insurance companies will refund all the premiums paid to the beneficiary plus 7-10% interest.

Guaranteed acceptance life insurance policies will immediately cover accidental causes of death, which include motor vehicle accidents, slips, and falls, natural disasters, etc.

What Types Of Burial Insurance Should I Avoid?

| PLANS TO AVOID | WHY? |

|---|---|

| Term life | Premiums increase after 5 years. Coverage ends after 80. |

| Pre-paid funeral plans | Expensive |

| Universal life | Tied with stocks |

| No health questions policies | With 2-year waiting period |

| Plans offering "teaser rates" | $9.95 per unit plans or $1 buys $100,000 coverage |

| Over priced plans | Insurance from TV and junk mail |

| Plans that accept mail-in payments | Risky |

| Plans that accept Direct Express | High lapse rate |

| Plans that accept Credit Cards | High lapse rate |

What Type Of Burial Insurance Is Best?

| FUNERAL FUNDS PLAN BENEFITS | INCLUDED |

|---|---|

| 1st Day Coverage | YES |

| Rates NEVER Increase | YES |

| Coverage NEVER Decreases | YES |

| Easy to get approved | YES |

| No Medical Exam | YES |

| Same Day Approval | YES |

| Death Claims Pay Fast | YES |

| Builds cash value | YES |

| Coverage Up To Age 121 | YES |

If I’m HIV Positive, Do I Need A Medical Exam To Qualify?

You are NOT required to take a medical exam to qualify for burial insurance for HIV-positive.

When you apply for burial insurance, you only have to answer basic questions about your health. The application process is simple; you don’t need to provide medical records or blood and urine samples.

You’ll get the official approval from the insurance company often within minutes!

How Much Insurance Do I Need If I’m HIV Positive?

The amount of burial insurance you should buy varies depending on your personal and financial circumstances. However, burial insurance should cover the cost of your funeral, burial, and final expenses.

The first step to figuring out how much burial insurance you need is to know your end-of-life expenses. Your funeral cost is often the biggest single expense you need to pay. Other end-of-life expenses to consider are your outstanding medical bills, living expenses, credit card bills, and other debts.

Here’s an example of a funeral cost breakdown from the National Funeral Directors Association.

| AVERAGE FUNERAL COST WITH VIEWING AND BURIAL | |

|---|---|

| Non-declinable basic services | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Hearse | $325 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Metal casket | $2,500 |

| Vault | $1,572 |

| Median Cost of a Funeral With Viewing and Burial | $9,420 |

| AVERAGE FUNERAL COST WITH VIEWING AND CREMATION | |

|---|---|

| Non-declinable basic services fee | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Cremation fee (if firm uses a third-party crematory) | $368 |

| Cremation Casket | $1,310 |

| Urn | $295 |

| Median Cost of a Funeral with Viewing and Cremation | $6,970 |

| Rental Casket | $995 |

| Alternate Cremation Container | $150 |

How Should I Pay My Premiums?

The best way to pay your premium is through a savings or checking account. We recommend you set a bank draft from your savings or checking account. That way, the bank will automatically pay your premium each month, and you don’t need to worry about your policy lapsing due to non-payment.

HIV And Burial Insurance Riders

Insurance policy riders add benefits to your policy. Adding insurance riders will enhance your policy to fit your needs. Some riders are built into your policy, while others can be added at an additional cost. Most riders are affordable, and it involves little to no underwriting.

Here’s a list of common burial insurance riders:

| FUNERAL FUNDS ADD-ONS | AVAILABILITY |

|---|---|

| Terminal Illness Add-On Benefit | Included with most plans |

| Nursing Home Care Add-On Benefit | Included with most plans |

Should You Tell The Life Insurance Company That You Are Hiv Positive?

You are required to disclose your current health status to an insurance company only when you are asked to divulge that information for coverage. You are not required to share your information if they do not ask about your HIV infection or any health-related issues.

You must be honest about health-related questions you are asked during a medical exam for HIV life insurance.

You must be aware that most life insurance policies have a contestability clause. It extends to two years after you bought the policy. During this period, your life insurance company can challenge a claim or cancel your policy if you are found to be lying about your health condition.

Why Do You Need To Buy Life Insurance If You Have Hiv?

HIV can cause AIDS, which results in failure of the immune system to combat life-threatening infections, leading to premature death.

Buying life insurance is imperative for an individual with HIV who is confronted with the harsh reality of death.

Buying life insurance can serve a different purpose. The first purpose of having life insurance for HIV-positive is to cover the final expenses. HIV life insurance can be used to pay funeral and burial costs and medical bills not covered by health insurance. It will ease the financial burden on the surviving family members.

Life insurance death benefits can also help replace your income if you pass away. Your beneficiaries can use the death benefit payout to pay off their mortgage or secure college educations for their children.

More often, people with HIV leave their families with massive medical debts to pay. Life insurance can provide a financial legacy for the survivors, which can be used to pay medical bills incurred before death. HIV burial insurance provides people with HIV with peace of mind knowing that their family will be taken care of after their death.

Can You Get Hiv Life Insurance If You Were Declined Due To HIV?

The good news is YES! You can still qualify for life insurance even if you were declined in the past. Tell us upfront if you were rejected by insurance companies specializing in HIV life insurance underwriting.

We need to know if the actual HIV life insurance program declined you or if you were declined before the company had an HIV program in place.

We will review the options available for you to help you get the protection you need. Call us at (888) 862-9456 if you have questions about HIV and insurance or if you have any questions about life insurance.

Benefits Of Burial & Funeral Insurance

Here are some of the benefits of purchasing a burial or funeral policy:

- No medical exam or doctor’s visit is required – easy to get approved.

- Ease of issue – easy to qualify and get insurance coverage.

- No Money Down to get approved – have your policy start whenever you want.

- Level premium – your premium will never increase.

- Fixed death benefit – your death benefit will never decrease for any reason.

- Permanent protection – your policy can not be canceled by the life insurance company if you continue to pay your premiums.

- Tax-free – the death benefit is directly paid to your beneficiary tax-free upon your death.

- Cash value builds up – burial insurance is a whole life policy that builds cash value over time.

Other Common Uses For Final Expense Life Insurance

All of these examples are appropriate uses for Final Expense Life Insurance:

- Burial insurance plan for HIV positive

- Cremation insurance plan for HIV positive

- Funeral home insurance plan for HIV positive

- Final Expense insurance plan for HIV positive

- Prepaid funeral plan insurance for HIV positive

- Mortgage payment protection plan for HIV positive

- Mortgage payoff life insurance plan for HIV positive

- Deceased spouse’s income replacement plan for HIV positive

- Legacy insurance gift plan to family or loved ones with HIV

- Medical or doctor bill life insurance plan for HIV positive

We can help you with any of the plans above. Your pricing will depend on your age, health, and coverage amount for each program option.

How Can Funeral Funds Help Me?

Finding a policy with AIDS, HIV, or AIDS-related complex needn’t be frustrating; working with an independent agency like Funeral Funds will make the process easier and quicker.

We will work with you every step to find the plan that fits your financial requirements and budget. You don’t have to waste your precious time searching for multiple insurance companies because we will do the work for you.

We work with many A+ rated insurance carriers that specialize in covering high-risk clients like you. We will search all those companies and match you up with the best burial insurance company that gives the best rate.

We will assist you in securing the coverage you need at a rate you can afford. So, if you are looking for Kidney Dialysis funeral insurance, or Kidney Dialysis burial insurance, or Kidney Dialysis life insurance, we can help.

Fill out our quote form on this page or call us at (888) 862-9456, and we can give you an accurate quote.

2 Comments

Jonathan P

My husband has had HIV for 7 years. His condition is stable with his current medications. He is 53 years old. Can he get life insurance through you guys?

Funeral Funds

Jonathan,

We do have some options for your husband. We would need to know a little bit more about his specific situation to best help you two out. Give us a call and we will help you understand your options.

Funeral Funds