2024 Burial Insurance with Huntington’s Disease

last updated on July 22, 2024

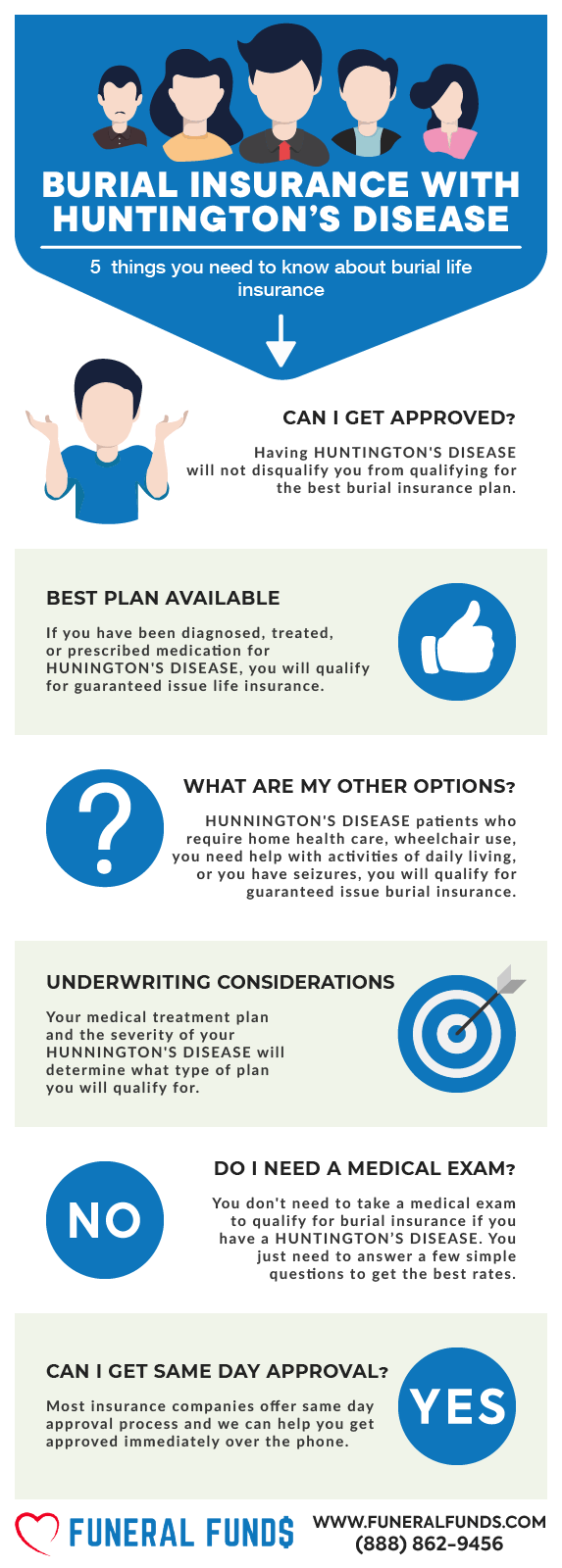

last updated on July 22, 2024Burial insurance with Huntington’s disease is possible, but having Huntington’s disease certainly narrows your funeral and burial insurance options.

!!! READ THIS FIRST !!!

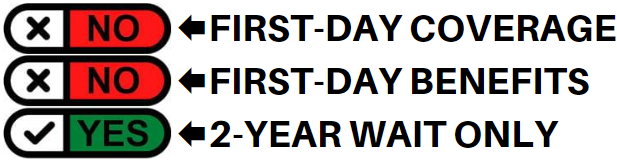

You can get a policy when you have Huntington’s disease, but what you must know is that no life insurance carrier will offer you coverage that protects you during the first 24 months (some plans will cover accidental death).

We recommend people with Huntington’s disease purchase a guaranteed issue life insurance that asks no health questions but does come with a 2-year waiting.

If you or a family member has been diagnosed with Huntington’s disease and would like more information about burial insurance, keep reading this article.

FOR EASIER NAVIGATION:

- What Is My Best Insurance Option If I Have a History of Huntington’s Disease?

- What Types of Burial Insurance Should I Avoid?

- What Type of Burial Insurance Is Best?

- If I Have Huntington’s Disease, Do I Need a Medical Exam to Qualify for Burial Insurance?

- Burial Insurance Underwriting If You Have Huntington’s Disease

- How Much Insurance Do I Need If I Have Huntington’s Disease?

- How Should I Pay My Premiums?

- Huntington’s Disease and Burial Insurance Riders

- Why Do I Need to Purchase Guaranteed Issue Life Insurance If I Have Huntington’s Disease?

- Benefits of Burial & Funeral Insurance

- Other Common Uses for Final Expense Life Insurance with Huntington’s Disease

- How Can Funeral Funds Help Me?

What Is My Best Insurance Option If I Have A History Of Huntington’s Disease?

If you have Huntington’s disease, then a guaranteed issue life insurance policy that asks no health questions is your best option.

Guaranteed issue policies don’t ask you about your medical history or current health. The insurance company will automatically approve your application, and the policy will take effect within a day.

You can qualify for a guaranteed final expense insurance policy if you are between the age of 40 and 85. You are a U.S citizen, and you live in a state where guaranteed issue policies are sold.

Guaranteed issue burial insurance has a 24-month graded period, but if you pass away in the first two years due to your Huntington’s disease, your beneficiary will receive your premiums plus 10% interest.

Your beneficiaries will also receive a full death benefit if you die from an accident or other catastrophic events in the first 24 months.

Best Option: Guaranteed issue burial insurance

HUNTINGTON’S DISEASE & ACTIVITIES OF DAILY LIVING

As Huntington’s disease progresses, the ability to care for oneself declines, and caregiving becomes increasingly necessary. As your disease progresses, you may need help from anyone with your activities of daily living. ADL includes eating, bathing, dressing, toileting, and taking medication. ADL will have a massive impact on the underwriting process.

Every single life insurance company will ask if you need help with activities of daily living.

Every final expense life insurance companies will flat out decline anyone needing help with their daily living activities. They will only offer you a guaranteed issue life insurance that costs a bit more and only pays out limited benefits during the first two years.

Best Option: Guaranteed issue burial insurance

THE DRAWBACKS OF GUARANTEED ISSUE BURIAL INSURANCE

White guaranteed issue final expense life insurance no exam is great, particularly for those with Huntington’s disease; they come with some disadvantages that you need to be fully aware of before considering to purchase the policy.

#1. Graded Death Benefits

With guaranteed issue life insurance there is where you need to remain alive for at least two years for it to cover death as a consequence of Huntington’s disease or other illnesses.

If you die during the waiting period, your beneficiary will only receive the return of the premium plus some interest, typically 10%. Once the two years have passed, your beneficiary would receive the full death benefit, even if it’s a day after.

Guaranteed issue life insurance will pay 100% of your death benefit if you die from an accident during the waiting period. Accidental deaths include motor vehicle accidents, slips, and falls, and natural disasters. Accidental death would be immediately covered and not subjected to the waiting period.

#2. Smaller Coverage Amounts

The death benefit is lower than traditional life insurance because the plan covers final expenses. Guaranteed issue policies only offer a maximum of $25,000 in coverage.

If you’re planning to buy several guaranteed issue policies from different insurers to get higher coverage than $25,000, you can do it, but you have to be aware that it will be expensive.

#3. More Expensive

Guaranteed issue life insurance policies are more expensive than traditional life insurance policies. The burial insurance carriers charge more because they take more risk in insuring people without knowing their medical condition.

What Types Of Burial Insurance Should I Avoid?

| PLANS TO AVOID | WHY? |

|---|---|

| Term life | Premiums increase after 5 years. Coverage ends after 80. |

| Pre-paid funeral plans | Expensive |

| Universal life | Tied with stocks |

| No health questions policies | With 2-year waiting period |

| Plans offering "teaser rates" | $9.95 per unit plans or $1 buys $100,000 coverage |

| Over priced plans | Insurance from TV and junk mail |

| Plans that accept mail-in payments | Risky |

| Plans that accept Direct Express | High lapse rate |

| Plans that accept Credit Cards | High lapse rate |

What Type Of Burial Insurance Is Best?

| FUNERAL FUNDS PLAN BENEFITS | INCLUDED |

|---|---|

| 1st Day Coverage | YES |

| Rates NEVER Increase | YES |

| Coverage NEVER Decreases | YES |

| Easy to get approved | YES |

| No Medical Exam | YES |

| Same Day Approval | YES |

| Death Claims Pay Fast | YES |

| Builds cash value | YES |

| Coverage Up To Age 121 | YES |

If I Have Huntington’s Disease, Do I Need A Medical Exam To Qualify For Burial Insurance?

You are NOT required to take a medical exam to qualify for burial insurance with Huntington’s disease.

When you apply for burial insurance, you only have to answer basic questions about your health. The application process is simple; you don’t need to provide medical records or blood and urine samples.

You’ll get the official approval from the insurance company often within minutes!

Burial Insurance Underwriting If You Have Huntington’s Disease

Burial insurance companies have two ways of underwriting:

FIRST – They may ask you a series of health questions. Your answers to their questions will determine your eligibility.

SECOND – They will electronically review your prescription history to verify your health.

When you have Huntington’s disease, you cannot qualify for any non-medical life insurance application that asks about your health history, health-related questions, or performs a prescription history check.

If you say yes to their questions about Huntington’s disease, they would outright decline your application. Similarly, if they find you have taken prescriptions for Huntington’s disease, they will decline your application even if you declare that you do not have Huntington’s disease.

There is no cure for Huntington’s disease, but there are ways to help manage the symptoms. Tetrabenazine and Deutetrabenazine will be prescribed to reduce chorea or involuntary movements, and antidepressant drugs to alleviate depression. Mood stabilizers and antipsychotic drugs can be given to help with some of the emotional disturbances.

Tetrabenazine is the only drug approved by the U.S. Food and Drug Administration to treat Huntington’s disease, and this drug is flagged for Huntington’s disease. If you have taken this drug, you will not qualify for any life insurance plan that has underwriting.

Even if you say no to the question about Huntington’s disease. The presence of Tetrabenazine in your prescription history will override your “no” answer.

How Much Insurance Do I Need If I Have Huntington’s Disease?

The amount of burial insurance you should buy varies depending on your personal and financial circumstances. However, burial insurance should cover the cost of your funeral, burial, and final expenses.

The first step to figuring out how much burial insurance you need is to know your end-of-life expenses. Your funeral cost is often the biggest single expense you need to pay. Other end-of-life expenses to consider are your outstanding medical bills, living expenses, credit card bills, and other debts.

Here’s an example of a funeral cost breakdown from the National Funeral Directors Association.

| AVERAGE FUNERAL COST WITH VIEWING AND BURIAL | |

|---|---|

| Non-declinable basic services | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Hearse | $325 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Metal casket | $2,500 |

| Vault | $1,572 |

| Median Cost of a Funeral With Viewing and Burial | $9,420 |

| AVERAGE FUNERAL COST WITH VIEWING AND CREMATION | |

|---|---|

| Non-declinable basic services fee | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Cremation fee (if firm uses a third-party crematory) | $368 |

| Cremation Casket | $1,310 |

| Urn | $295 |

| Median Cost of a Funeral with Viewing and Cremation | $6,970 |

| Rental Casket | $995 |

| Alternate Cremation Container | $150 |

How Should I Pay My Premiums?

The best way to pay your premium is through a savings or checking account. We recommend you set a bank draft from your savings or checking account. That way, the bank will automatically pay your premium each month, and you don’t need to worry about your policy lapsing due to non-payment.

Huntington’s Disease And Burial Insurance Riders

Insurance policy riders add benefits to your policy. Adding insurance riders will enhance your policy to fit your needs. Some riders are built into your policy, while others can be added at an additional cost. Most riders are affordable, and it involves little to no underwriting.

Here’s a list of common burial insurance riders:

| FUNERAL FUNDS ADD-ONS | AVAILABILITY |

|---|---|

| Terminal Illness Add-On Benefit | Included with most plans |

| Nursing Home Care Add-On Benefit | Included with most plans |

Why Do I Need To Purchase Guaranteed Issue Life Insurance If I Have Huntington’s Disease?

Huntington’s disease is an inherited neurological disease that causes brain cells to die in various areas of the brain, including those that control voluntary movement. The condition gets worse over time.

There is no known cure for Huntington’s disease, and there is no effective treatment discovered to stop the progression of this disease. The life expectancy of people with Huntington’s disease is 10 to 20 years.

Huntington’s disease affects the whole body. Over time the symptoms associated with the disease will overpower your body. This makes qualifying for a traditional term or whole life insurance policy impossible.

For a Huntington’s patient confronted with the reality of death, buying burial insurance is a must. The sooner you buy a life insurance policy, the better because of the two-year graded period.

The sooner your two-year waiting period is over, the sooner you will have 100% coverage.

If you just received a recent diagnosis, there is a good chance that you will outlive the two-year waiting period if you start immediately. You will also save on premium if you apply now because your monthly premium is computed based on your current age.

Buying guaranteed issue life insurance can provide financial protection to your family when you pass away. It can be used to cover your final expenses. A funeral is expensive and can cost over $10,000. Huntington’s life insurance payout can be used to pay for your funeral and burial costs.

More often, people with Huntington’s disease leave their families with massive medical debts to pay. A guaranteed issue policy can provide a source of funds to pay those medical debts incurred before death. Purchasing a guaranteed issue policy will give you peace of mind from knowing that your family will be taken care of upon death.

BENEFITS OF BURIAL & FUNERAL INSURANCE

Here are some of the benefits of purchasing a burial or funeral policy:

- No medical exam or doctor’s visit is required – easy to get approved.

- Ease of issue – easy to qualify and get insurance coverage.

- No Money Down to get approved – have your policy start whenever you want.

- Level premium – your premium will never increase.

- Fixed death benefit – your death benefit will never decrease for any reason.

- Permanent protection – your policy can not be canceled by the life insurance company if you continue to pay your premiums.

- Tax-free – the death benefit is directly paid to your beneficiary tax-free upon your death.

- Cash value builds up – burial insurance is a whole life policy that builds cash value over time.

Other Common Uses For Final Expense Life Insurance With Huntington’s Disease

All of these examples are appropriate uses for Final Expense Life Insurance:

- Burial insurance plan with Huntington’s disease

- Cremation insurance plan with Huntington’s disease

- Funeral home insurance plan with Huntington’s disease

- Final Expense insurance plan with Huntington’s disease

- Prepaid funeral plan insurance with Huntington’s disease

- Mortgage payment protection plan with Huntington’s disease

- Mortgage payoff life insurance plan with Huntington’s disease

- Deceased spouse’s income replacement plan with Huntington’s disease

- Legacy insurance gift plan to family or loved ones with Huntington’s disease

- Medical or doctor bill life insurance plan with Huntington’s disease

We can help you with any of the plans above. Your pricing will depend on your age, health, and coverage amount for each program option.

How Can Funeral Funds Help Me?

Finding a policy with Huntington’s disease needn’t be frustrating; working with an independent agency like Funeral Funds will make the process easier and quicker.

We will work with you every step to find the plan that fits your financial requirements and budget. You need not waste your precious time searching for multiple insurance companies because we will do the dirty work for you.

We work with many A+ rated insurance carriers that specialize in covering high-risk clients like you. We will search all those companies and match you up with the best burial insurance company that gives the best rate.

We will assist you in securing the coverage you need at a rate you can afford. So, if you are looking for Huntington’s disease funeral insurance, Huntington’s disease burial insurance, or Huntington’s disease life insurance, we can help. Fill out our quote form on this page or call us at (888) 862-9456, and we can give you an accurate quote.