2024 Burial Insurance with a Defibrillator

last updated on July 22, 2024

last updated on July 22, 2024If you’re looking for burial insurance with a defibrillator, you need to keep reading. If you want a burial policy and you have issues regarding your heart, the good news is that you would still be able to get the coverage you want at an affordable price.

Because you have an implanted defibrillator, the insurance companies will want to know more about your unique medical condition and treatments before issuing you a policy.

In this article, we will show you how burial insurance carriers underwrite applicants with a defibrillator implant, what policy options are open for you, and how you can get the best burial insurance with a defibrillator.

FOR EASIER NAVIGATION:

- What Is My Best Insurance Option If I Have a Defibrillator?

- What Types of Burial Insurance Should I Avoid?

- What Type of Burial Insurance Is Best?

- If I Have a Defibrillator, Do I Need A Medical Exam to Qualify for Burial Insurance?

- Burial Insurance Underwriting If You Have a Defibrillator

- How Much Insurance Do I Need If I Have a Defibrillator?

- How Should I Pay My Premiums?

- Defibrillator and Burial Insurance Riders

- Information We Need if You Have a Defibrillator

- How to Get the Best Burial Insurance Rates for People with Defibrillator

- Benefits of Burial & Funeral Insurance

- Other Common Uses for Final Expense Life Insurance with a Defibrillator

- How Can Funeral Funds Help Me?

- Additional Questions & Answers On Burial Insurance With Defibrillator

What Is My Best Insurance Option If I Have A Defibrillator?

How long your defibrillator was implanted will be essential in determining your insurance eligibility.

DEFIBRILLATOR IMPLANTED OVER 2 YEARS AGO

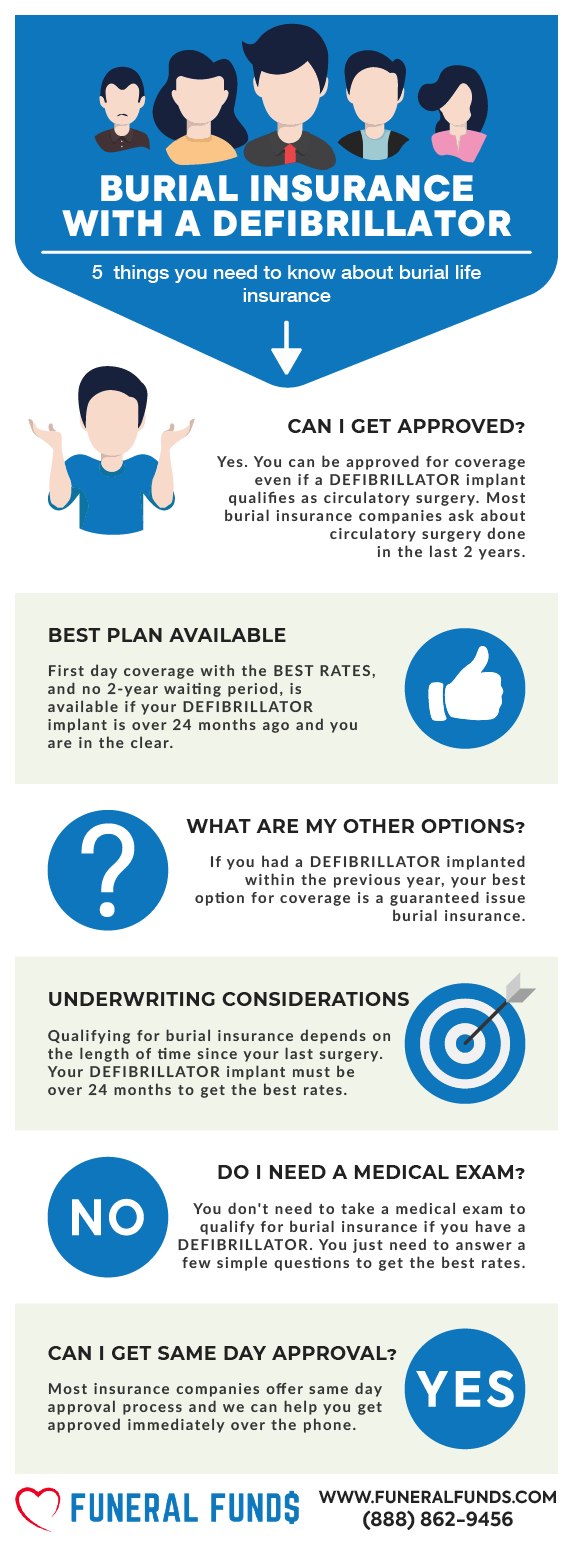

An implantable cardioverter defibrillator (ICD) is also is also called automatic internal cardiac defibrillator. ICD’s are implanted directly into the patient’s chest or abdomen to protect them from sudden death. A defibrillator implant qualifies as circulatory surgery.

You are in the clear if your defibrillator implant is over 24 months ago. You can easily qualify for a level death benefit plan with first-day coverage from dozens of burial insurance companies.

Your rates will be comparable to people in perfect health, and you will be fully protected from day one. You will also qualify for the lowest premium.

Best Option: Level death benefit plan with first-day coverage

DEFIBRILLATOR IMPLANTED WITHIN 24 MONTHS

If your defibrillator was implanted within the last two years, your best burial insurance option is a first-day benefit plan.

The first-day benefit plan provides first-day coverage, and the death benefit is phased in over time.

Best Option: First-day benefit plan

DEFIBRILLATOR BATTERY CHANGES

A defibrillator battery change is considered simple outpatient surgery.

Some insurance companies may consider this procedure a heart or circulatory surgery resulting in a waiting period and higher premiums if your surgery is very recent.

The good news is that we have burial insurance companies that don’t consider a defibrillator battery change as heart surgery. If your battery change is just recent, we can put you with one of those companies to be able to get the first-day coverage without the waiting period.

Best Option: Level death benefit plan with first-day coverage

What Types Of Burial Insurance Should I Avoid?

| PLANS TO AVOID | WHY? |

|---|---|

| Term life | Premiums increase after 5 years. Coverage ends after 80. |

| Pre-paid funeral plans | Expensive |

| Universal life | Tied with stocks |

| No health questions policies | With 2-year waiting period |

| Plans offering "teaser rates" | $9.95 per unit plans or $1 buys $100,000 coverage |

| Over priced plans | Insurance from TV and junk mail |

| Plans that accept mail-in payments | Risky |

| Plans that accept Direct Express | High lapse rate |

| Plans that accept Credit Cards | High lapse rate |

What Type Of Burial Insurance Is Best?

| FUNERAL FUNDS PLAN BENEFITS | INCLUDED |

|---|---|

| 1st Day Coverage | YES |

| Rates NEVER Increase | YES |

| Coverage NEVER Decreases | YES |

| Easy to get approved | YES |

| No Medical Exam | YES |

| Same Day Approval | YES |

| Death Claims Pay Fast | YES |

| Builds cash value | YES |

| Coverage Up To Age 121 | YES |

If I Have A Defibrillator, Do I Need A Medical Exam To Qualify For Burial Insurance?

You are NOT required to take a medical exam to qualify for burial insurance with a defibrillator.

When you apply for burial insurance, you only have to answer some basic questions about your health. The application process is simple; you don’t need to provide medical records or blood and urine samples.

You’ll get the official approval from the insurance company often within minutes!

Burial Insurance Underwriting If You Have A Defibrillator

Burial insurance companies have two ways of underwriting:

FIRST – They may ask you a series of health questions. Your answers to their questions will determine your eligibility.

SECOND – They will electronically review your prescription history to verify your health.

A defibrillator implant qualifies as circulatory surgery. Most burial insurance companies ask about recent circulatory surgery. Most questions center around surgeries within the last 24. It’s very seldom to see them ask beyond the 2-year mark.

HEATH QUESTIONS:

- Prior to age 50 or during the past 24 months, have you been hospitalized for heart or circulatory surgery (including pacemaker, heart valve replacement, bypass, angioplasty, stent implant, or any procedure to improve circulation to the heart or brain?

- Within the past 24 months, have you been treated or hospitalized for heart or circulatory surgery (including pacemaker, bypass, heart valve replacement, angioplasty, stent implant, or any procedure to improve circulation to the heart or brain?

- Within the past 2 years, have you had or been diagnosed with angina, heart attack, cardiomyopathy, or any type of heart or circulatory surgery?

Generally, qualifying for burial insurance or final expense insurance depends on the length of time since your last surgery. If your defibrillator implant is very recent, it may impact your premium and whether or not you will have a waiting period on your policy.

PRESCRIPTION HISTORY CHECK

The insurance companies will also review your prescription history as part of their underwriting procedure and risk analysis.

If you are taking prescription medication for other heart issues associated with your defibrillator, this may impact what plans and rates you qualify for.

How Much Insurance Do I Need If I Have A Defibrillator?

The amount of burial insurance you should buy varies depending on your personal and financial circumstances. However, burial insurance should cover the cost of your funeral, burial, and final expenses.

The first step to figuring out how much burial insurance you need is to know your end-of-life expenses. Your funeral cost is often the biggest single expense you need to pay. Other end-of-life expenses to consider are your outstanding medical bills, living expenses, credit card bills, and other debts.

Here’s an example of a funeral cost breakdown from the National Funeral Directors Association.

| AVERAGE FUNERAL COST WITH VIEWING AND BURIAL | |

|---|---|

| Non-declinable basic services | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Hearse | $325 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Metal casket | $2,500 |

| Vault | $1,572 |

| Median Cost of a Funeral With Viewing and Burial | $9,420 |

| AVERAGE FUNERAL COST WITH VIEWING AND CREMATION | |

|---|---|

| Non-declinable basic services fee | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Cremation fee (if firm uses a third-party crematory) | $368 |

| Cremation Casket | $1,310 |

| Urn | $295 |

| Median Cost of a Funeral with Viewing and Cremation | $6,970 |

| Rental Casket | $995 |

| Alternate Cremation Container | $150 |

How Should I Pay My Premiums?

The best way to pay your premium is through a savings or checking account. We recommend you set a bank draft from your savings or checking account. That way, the bank will automatically pay your premium each month, and you don’t need to worry about your policy lapsing due to non-payment.

Defibrillator And Burial Insurance Riders

Insurance policy riders add benefits to your policy. Adding insurance riders will enhance your policy to fit your needs. Some riders are built into your policy, while others can be added at an additional cost. Most riders are affordable, and it involves little to no underwriting.

Here’s a list of common burial insurance riders:

| FUNERAL FUNDS ADD-ONS | AVAILABILITY |

|---|---|

| Terminal Illness Add-On Benefit | Included with most plans |

| Nursing Home Care Add-On Benefit | Included with most plans |

Information We Need If You Have A Defibrillator

When applying for final expense insurance with a defibrillator, it is important to provide us much information as possible. We will ask you a series of health questions to better understand your condition.

These questions include:

- When was your ICD installed?

- Why do you need a defibrillator?

- When was the last time you had a battery change?

- What other health conditions do you have?

- What prescription medications do you take, and for what condition?

We need to know your medical condition to provide you with the best recommendation. The more information we get, the better our chances of finding affordable insurance coverage.

How To Get The Best Burial Insurance Rates For People With Defibrillators

To find affordable coverage after your defibrillator implant, you must contact an independent insurance agency that works with the right type of insurance companies looking more favorably at defibrillators.

We know about the insurance companies underwriting guidelines and requirements for burial insurance coverage with a defibrillator. We will shop your case with multiple companies to match you with the best plan and the most affordable rate. We will do our best to get you the lowest cost coverage for your condition.

So, if you are looking for burial insurance with a defibrillator implant, we can help.

Benefits Of Burial & Funeral Insurance

Here are some of the benefits of purchasing a burial or funeral policy:

- No medical exam or doctor’s visit is required – easy to get approved.

- Ease of issue – easy to qualify and get insurance coverage.

- No Money Down to get approved – have your policy start whenever you want.

- Level premium – your premium will never increase.

- Fixed death benefit – your death benefit will never decrease for any reason.

- Permanent protection – your policy can not be canceled by the life insurance company if you continue to pay your premiums.

- Tax-free – the death benefit is directly paid to your beneficiary tax-free upon your death.

- Cash value builds up – burial insurance is a whole-life policy that builds cash value over time.

Other Common Uses For Final Expense Life Insurance With A Defibrillator

All of these examples are appropriate uses for Final Expense Life Insurance:

- Burial insurance plan with a defibrillator

- Cremation insurance plan with a defibrillator

- Funeral home insurance plan with a defibrillator

- Final Expense insurance plan with a defibrillator

- Prepaid funeral plan insurance with a defibrillator

- Mortgage payment protection plan with a defibrillator

- Mortgage payoff life insurance plan with a defibrillator

- Deceased spouse’s income replacement plan with a defibrillator

- Legacy insurance gift plan to family or loved ones with a defibrillator

- Medical or doctor bill life insurance plan with a defibrillator

We can help you with any of the plans above. Your pricing will depend on your age, health, and coverage amount for each program option.

How Can Funeral Funds Help Me?

Finding a policy with a defibrillator needn’t be frustrating, but working with an independent agency like Funeral Funds will make the process easier and quicker.

We will work with you every step to find the plan that fits your financial requirements and budget. You need not waste your precious time searching for multiple insurance companies because we will do the dirty work for you.

We work with many A+ rated insurance carriers that specialize in covering high-risk clients like you. We will search all those companies and match you up with the best burial insurance company that gives the best rate.

We will assist you in securing the coverage you need at a rate you can afford. So, if you are looking for funeral or burial insurance with a defibrillator, we can help.

Fill out our quote form on this page or call us at (888) 862-9456, and we can give you an accurate quote.

Additional Questions & Answers On Burial Insurance With A Defibrillator

Can you get life insurance if you have a defibrillator?

Yes, you can get life insurance with a defibrillator. Many insurance companies consider having a defibrillator to be a minor health condition and will not charge you more for life insurance because of it. However, most insurers will likely decline your application if you have had a recent heart attack or stroke.

What heart conditions require a defibrillator?

A defibrillator is most commonly used to treat cardiac arrest, which is a condition in which the heart stops beating. However, a defibrillator may also treat other heart conditions, such as ventricular tachycardia or fibrillation.

Is a defibrillator implant considered surgery in life insurance?

Yes, a defibrillator implant is considered surgery in life insurance.

Is a defibrillator use a pre-existing condition for life insurance?

No, defibrillator use is not a pre-existing condition for life insurance. Many insurers consider it to be a minor health condition. However, life insurance companies want to know why you need a defibrillator.

Do I need to tell insurance about my defibrillator use?

Yes, you need to tell your insurance company about your defibrillator use. Failure to disclose this information could lead to denied claims or increased premiums in the future.

Can a person with ICD get burial insurance?

Yes, a person with an ICD can get burial insurance. Most insurers will not consider having an ICD to be a major health condition and will not charge you more for burial insurance because of it. However, most insurers will likely decline your application if you have had a recent heart attack or stroke.

Do I need to take a medical exam if I have a defibrillator?

No, you do not need to take a medical exam if you have a defibrillator. However, you may need to provide your insurer with information about your defibrillator and why you need it.

Is there an age limit for burial insurance with defibrillators?

Most life insurance companies accept applicants up to 85 years old.

Can I get insurance if I have a defibrillator and use blood thinners?

Yes, you can get life insurance with a defibrillator if you are using blood thinners. Many insurers consider having a defibrillator to be a minor health condition and will not charge you more for life insurance because of it. However, most insurers will likely decline your application if you have had a recent heart attack or stroke.

Can you get first-day coverage insurance if you have a defibrillator?

Yes, you can get first-day coverage insurance if you have a defibrillator. However, your insurer will likely want to know why you need a defibrillator.

What is the life expectancy of someone with a defibrillator?

The life expectancy of someone with a defibrillator varies depending on the person’s health condition. However, most people with a defibrillator live normal, healthy lives.

What are the things that may affect my eligibility if I have a defibrillator?

There are several things that may affect your eligibility for life insurance if you have a defibrillator. These include, but are not limited to, having a recent heart attack or stroke, using blood thinners, and the time that passed since your defibrillator implant.

Is it harder to get life insurance if you have a defibrillator?

No, it is not harder to get life insurance if you have a defibrillator. Many insurers consider having a defibrillator to be a minor health condition and will not charge you more for life insurance because of it.

What is the life expectancy after defibrillator surgery?

The life expectancy after defibrillator surgery varies depending on the person’s health condition. However, most people with a defibrillator implant live normal, healthy lives.

Which insurance is best for patients with defibrillators?

There is no one-size-fits-all answer to this question. However, most life insurance companies will not consider having a defibrillator a major health condition and will not charge you more for life insurance because of it.

Do I need to disclose that I have a defibrillator when I apply for insurance?

Yes, you must disclose that you have a defibrillator when applying for insurance. Failure to disclose this information could lead to denied claims or increased premiums in the future.

Can I qualify for cremation insurance with a defibrillator?

Yes, you can qualify for cremation insurance with a defibrillator. Most insurers will not consider having an ICD to be a major health condition and will not charge you more for cremation insurance because of it. However, most insurers will likely decline your application if you have had a recent heart attack or stroke.

Is having an ICD a disability?

No, having an ICD is not a disability. However, people with disabilities may be able to get life insurance with a defibrillator.

How do you get life insurance after defibrillator installation?

Getting life insurance after a defibrillator installation is like getting life insurance if you have been healthy. Consult a life insurance agent from Funeral Funds to make the process easier.

What is my best insurance option if I have a defibrillator?

First-day coverage is the best option for people with a defibrillator. You can easily qualify for this plan if your defibrillator surgery has been two years or longer.

Is defibrillator installation fatal in life insurance?

No, defibrillator installation is not fatal in life insurance. Many insurers consider having a defibrillator a minor health condition and will not charge you more for life insurance because of it.

Can you be denied insurance for a defibrillator?

Yes, some life insurance companies will not accept your application if your defibrillator implant is very recent.

What are the things that may affect my eligibility if I have a defibrillator?

There are some things that may affect your eligibility for life insurance if you have a defibrillator. These include, but are not limited to, having a recent heart attack or stroke, using blood thinners, and the time that passed since your defibrillator implant.

Is there a waiting period for life insurance with a defibrillator?

Most life insurance offers a first-day coverage plan to those who have had their defibrillator implant for two years or longer.

Can defibrillator use affect your life insurance rates?

No, defibrillator use will not affect your life insurance rates. Many insurers consider having a defibrillator a minor health condition and will not charge you more for life insurance.

What are the premiums for burial insurance with defibrillators?

The premiums for burial insurance with defibrillators vary depending on the insurer.

What is the average cost of life insurance for someone with a defibrillator?

The average cost of life insurance for someone with a defibrillator may vary depending on the insurer, your age, and other health conditions you may have.

Can defibrillator users get final expense insurance?

Yes, most insurers will not consider having an ICD to be a major health condition and will not charge you more for final expense insurance because of it. However, most insurers will likely decline your application if you have had a recent heart attack or stroke.

Can defibrillator use affect life insurance?

No, defibrillator use will not affect your life insurance. Many insurers consider having a defibrillator a minor health condition and will not charge you more for life insurance.

Can you be rejected for life insurance because of a defibrillator?

Yes, some life insurance companies will not accept your application if you have a recent defibrillator implant.

How can you get the best life insurance rates with a defibrillator?

Consult a life insurance agent from Funeral Funds to get the best life insurance rates with a defibrillator. Our agents are experts in finding the right life insurance policy for you, regardless of your health condition.

What is the best insurance option for people with defibrillators?

First-day coverage is the best option for people with a defibrillator. You can easily qualify for this plan if your defibrillator surgery is two years or longer.

What are the best life insurance companies for defibrillators?

Each life insurance company has different underwriting criteria, so it is important to consult with an agent from Funeral Funds to find the best life insurance company for you.

What are some tips for getting life insurance with a defibrillator?

Here are some tips for getting life insurance with a defibrillator:

- Consult an agent from Funeral Funds to find the best life insurance policy for you.

- Get a first-day coverage plan to ensure that you are fully covered.

- Ensure that your insurer considers having a defibrillator a minor health condition.

- Be honest about your health condition when applying for life insurance.

- Most insurers will likely decline your application if you have had a recent heart attack or stroke.