2024 Burial Insurance with a Heart Transplant [Use Caution]

last updated on July 22, 2024

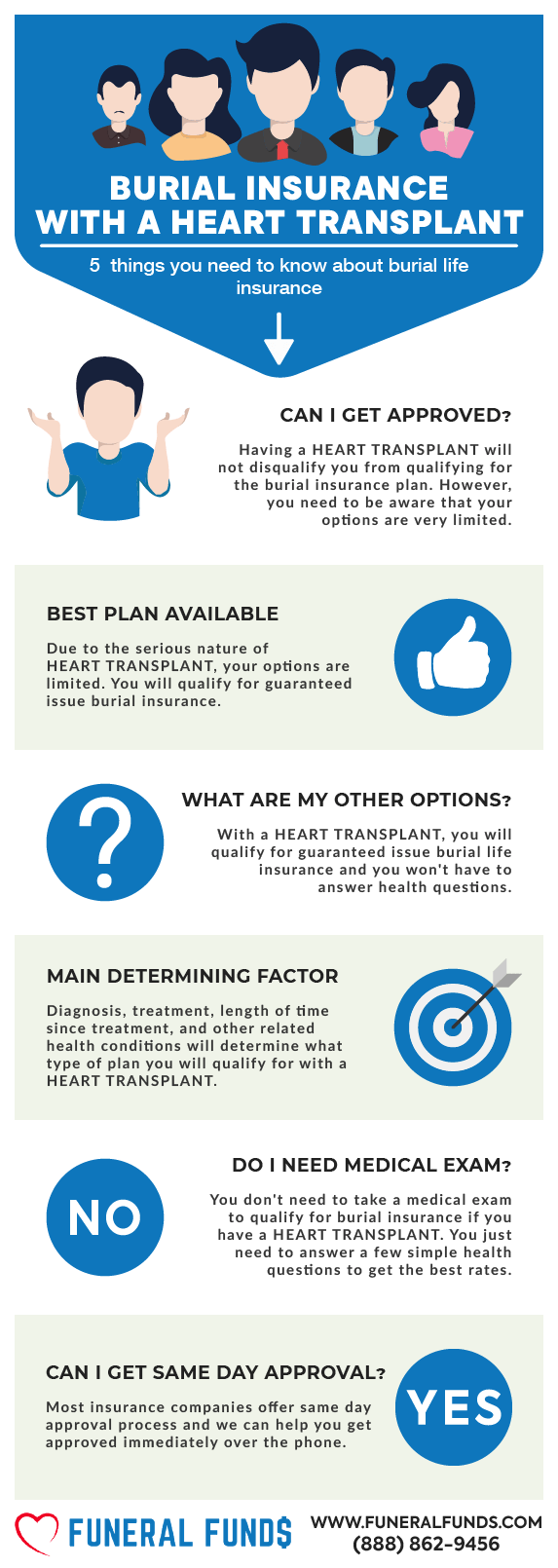

last updated on July 22, 2024You can get approved for burial insurance with a heart transplant. However, your burial insurance plan will always have a two-year waiting period.

!!! READ THIS FIRST !!!

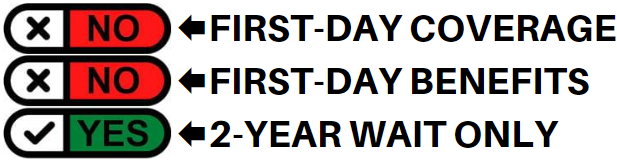

It is important to mention that it is impossible to qualify for a plan with first-day coverage because of the extremely high risks involved with your heart transplant.

We recommend people who have had organ transplant purchase a guaranteed issue life insurance that asks no health questions but does come with a 2-year waiting.

In this article, we will answer many of the questions that you may have about what options are open for you if you had a heart transplant and how to find the best plan for your needs.

FOR EASIER NAVIGATION:

- What Is My Best Insurance Option If I Have a History of Heart Transplant?

- Should I Buy a Guaranteed Issue Policy If I Had a Heart Transplant?

- The Best Guaranteed Issue Life Insurance Policy

- What Types of Burial Insurance Should I Avoid?

- What Type of Burial Insurance Is Best?

- If I Have a Heart Transplant, Do I Need a Medical Exam to Qualify for Burial Insurance?

- Burial Insurance Underwriting If You Have Heart a Transplant

- How Much Insurance Do I Need If I Have a Heart Transplant?

- How Should I Pay My Premiums?

- Heart Transplant and Burial Insurance Riders

- Other Common Uses for Final Expense Life Insurance with a Heart Transplant

- How Can Funeral Funds Help Me?

What Is My Best Insurance Option If I Have A History Of Heart Transplant?

Life insurance companies care about heart transplants because having a heart transplant can significantly decrease your life expectancy. Due to the serious nature of heart transplants, there is only one option for life insurance coverage. This option is called guaranteed issue burial insurance with a two-year waiting period.

Having a heart transplant means you will need to live for two years before the insurance company will pay the 100% death benefit to your beneficiaries (for any medical reasons).

If you were to die during the waiting period, the company would just refund all your premiums plus 10% interest (unless it was an accident, and then they will pay your full coverage amount in full).

Best Option: Guaranteed issue burial insurance

You will qualify for guaranteed issue burial insurance even if you say yes to the following questions:

- Do you have a heart transplant?

- Did you have any complications after the heart transplant?

- Have your doctor told you that you might not live more than a few months after your surgery?

Under these circumstances, you will still be eligible for a guaranteed acceptance or issue policy.

You will need to meet the following requirements to get approved:

- You are a U.S. citizen

- You meet the age requirements of 50-85 years old

- You live in a state where guaranteed issue life insurance policies are available.

WHAT IS A GUARANTEED ISSUE BURIAL INSURANCE?

It is also called no-exam no-questions-asked life insurance or guaranteed acceptance life insurance for transplant patients. It is whole life insurance that lasts the rest of your lifetime.

The application is straightforward. You only need to fill out your personal, beneficiary, and payment information. You can sign your name on the application over the phone or on the computer and send it, and you will be approved for coverage in a matter of minutes.

These policies are blessings for heart transplant recipients because there are no medical exam or health questions.

BENEFITS OF GUARANTEED ISSUE BURIAL INSURANCE

- No health questions – This is the most significant advantage for heart transplant recipients because you’re guaranteed to be approved, and no questions are asked and no medical exam either.

- Easy to qualify – It’s a simple yes or no application. The insurance company will not perform a medical exam, put your medical records or look at your prescription history. You will be approved immediately by most companies.

- Fixed monthly premium – Your monthly insurance bill will never increase; your premium is locked in your current age and will remain fixed for the rest of your life. As long as you keep paying your monthly premiums, it will never increase under any circumstances.

- Not Cancelable – Some people complain about their life insurance canceling because of their worsening health condition. Guaranteed issue burial insurance for heart transplant patients will never cancel because of declining health or advancing age.

- The death benefit will never decrease – Your death benefit has a fixed rate and guaranteed to never decrease for any reason. Your beneficiaries will receive your full death benefit when you pass away after the two-year waiting period.

- Cash value accumulation – Guaranteed acceptance burial insurance is whole life insurance that accumulates cash value over time. It can be used to pay your premiums, or you can borrow against it to be used for any purpose.

These are the benefits of a guaranteed life insurance policy. Once you are over the two-year waiting period, you are covered for a natural cause of death. You take out the policy and make the first payment, you are fully covered for accidental death from the first day.

Should I Buy A Guaranteed Issue Policy If I Had A Heart Transplant?

When you have a heart transplant, you will not qualify for anything other than guaranteed issue life insurance with a waiting period. You might ask: “Why do I need to get a plan like that if it doesn’t cover me from the first day?”

All heart transplant recipients take immunosuppressant, anti-rejection, and other “knock-out” medications for every company.

Your only option for life insurance coverage is guaranteed issue burial insurance. There’s no other way to get any type of 1st-day life insurance coverage.

Here’s why we recommend guaranteed acceptance life insurance for those who have heart transplants:

- There could be a complication from your operation.

- You could have a heart attack.

- You could develop other health conditions like high blood pressure or diabetes.

- Your doctor may prescribe other medications that are flagged by the life insurance company.

Other health conditions may also prevent you from qualifying for immediate coverage. Guaranteed issue burial insurance is the only option. You should act now, buy a guaranteed issue plan, and work on the waiting period.

Bottom line: The sooner you work on the waiting period the sooner you will get full coverage.

The Best Guaranteed Issue Life Insurance Policy

The best insurance for transplant patients will not make you wait more than two years to get you fully covered.

Some companies offer plans that have three or even four-year waiting periods. 3 and 4-year wait policies are absolute garbage and should be rejected immediately if they are proposed to you! Avoid these plans at all costs.

Two years is the shortest period possible before you are fully covered. You should never have to wait longer than that.

There are no health questions and no medical exams. If you pass away during the first two years as a consequence of your heart transplant, your beneficiaries will get the return of your premiums plus 10%.

What Types Of Burial Insurance Should I Avoid?

| PLANS TO AVOID | WHY? |

|---|---|

| Term life | Premiums increase after 5 years. Coverage ends after 80. |

| Pre-paid funeral plans | Expensive |

| Universal life | Tied with stocks |

| No health questions policies | With 2-year waiting period |

| Plans offering "teaser rates" | $9.95 per unit plans or $1 buys $100,000 coverage |

| Over priced plans | Insurance from TV and junk mail |

| Plans that accept mail-in payments | Risky |

| Plans that accept Direct Express | High lapse rate |

| Plans that accept Credit Cards | High lapse rate |

What Type Of Burial Insurance Is Best?

| FUNERAL FUNDS PLAN BENEFITS | INCLUDED |

|---|---|

| 1st Day Coverage | YES |

| Rates NEVER Increase | YES |

| Coverage NEVER Decreases | YES |

| Easy to get approved | YES |

| No Medical Exam | YES |

| Same Day Approval | YES |

| Death Claims Pay Fast | YES |

| Builds cash value | YES |

| Coverage Up To Age 121 | YES |

If I Have A Heart Transplant, Do I Need A Medical Exam To Qualify For Burial Insurance?

You are NOT required to take a medical exam to qualify for burial insurance with a heart transplant.

When you apply for burial insurance, you only have to answer some basic questions about your health. The application process is simple; you don’t need to provide medical records or blood and urine samples.

You’ll get the official approval from the insurance company often within minutes!

Burial Insurance Underwriting If You Have A Heart Transplant

Underwriting is the procedure used by insurance carriers to determine your level of risk and to assess if you will qualify for burial insurance.

Burial insurance companies have two ways of underwriting:

FIRST – They may ask you a series of health questions. Your answers to their questions will determine your eligibility.

SECOND – They will electronically review your prescription history to verify your health.

HEALTH QUESTIONS

Every burial insurance company will ask about heart transplants. Here are some common questions:

- Have you been treated for or diagnosed or been advised by a physician to have an organ transplant?

- Have you had, or been advised to have by a member of the medical profession, an organ transplant, or have you been diagnosed as having a terminal illness?

- Have you ever received, or been advised to receive, an organ or bone marrow transplant?

Most life insurance companies with underwriting (health questions) will ask these questions in the “knockout” section. If you answer any of the questions with a “YES” in a knockout section, you will not qualify for an immediate coverage plan.

PRESCRIPTION HISTORY CHECK

When you had a heart transplant, your body will not readily accept the newly transplanted organ. It will consider your new heart as a foreign body. Your body will attack the new heart and try to destroy it as it considers it a foreign invader.

As a result, you will be prescribed immunosuppressant drugs for your heart transplant. The immunosuppressant drugs will suppress the body’s ability to fight the new organ. These anti-rejection drugs minimize the operation’s side effects and produce effective immunosuppression.

Some immunosuppressant drugs cause a red flag to life insurance carriers. If you take any of these drugs for your heart transplant, you will be flagged as a heart transplant recipient and considered a high-risk applicant.

Here’s a list of common heart transplant medications:

- Azathioprine

- Basiliximab (Simulect)

- Belatacept

- Calcineurin

- Cyclosporine

- Daclizumab

- Muromonab-CD3

- Mycophenolate Mofetil (CellCept)

- Mycophenolic acid (Myfortic)

- Prednisone

- Sirolimus (Rapamune)

- Tacrolimus

- Thymoglobin

Taking any of these drugs will indicate to the insurance company that you are an organ transplant recipient.

How Much Insurance Do I Need If I Have A Heart Transplant?

The amount of burial insurance you should buy varies depending on your personal and financial circumstances. However, burial insurance should cover the cost of your funeral, burial, and final expenses.

The first step to figuring out how much burial insurance you need is to know your end-of-life expenses. Your funeral cost is often the biggest single expense you need to pay. Other end-of-life expenses to consider are your outstanding medical bills, living expenses, credit card bills, and other debts.

Here’s an example of a funeral cost breakdown from the National Funeral Directors Association.

| AVERAGE FUNERAL COST WITH VIEWING AND BURIAL | |

|---|---|

| Non-declinable basic services | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Hearse | $325 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Metal casket | $2,500 |

| Vault | $1,572 |

| Median Cost of a Funeral With Viewing and Burial | $9,420 |

| AVERAGE FUNERAL COST WITH VIEWING AND CREMATION | |

|---|---|

| Non-declinable basic services fee | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Cremation fee (if firm uses a third-party crematory) | $368 |

| Cremation Casket | $1,310 |

| Urn | $295 |

| Median Cost of a Funeral with Viewing and Cremation | $6,970 |

| Rental Casket | $995 |

| Alternate Cremation Container | $150 |

How Should I Pay My Premiums?

The best way to pay your premium is through a savings or checking account. We recommend you set a bank draft from your savings or checking account. That way, the bank will automatically pay your premium each month, and you don’t need to worry about your policy lapsing due to non-payment.

Heart Transplant And Burial Insurance Riders

Insurance policy riders add benefits to your policy. Adding insurance riders will enhance your policy to fit your needs. Some riders are built into your policy, while others can be added at an additional cost. Most riders are affordable, and it involves little to no underwriting.

Here’s a list of common burial insurance riders:

| FUNERAL FUNDS ADD-ONS | AVAILABILITY |

|---|---|

| Terminal Illness Add-On Benefit | Included with most plans |

| Nursing Home Care Add-On Benefit | Included with most plans |

Other Common Uses For Final Expense Life Insurance With A Heart Transplant

All of these examples are appropriate uses for Final Expense Life Insurance:

- Burial insurance plan with a heart transplant

- Cremation insurance plan with a heart transplant

- Funeral home insurance plan with a heart transplant

- Final Expense insurance plan with a heart transplant

- Prepaid funeral plan insurance with a heart transplant

- Mortgage payment protection plan with a heart transplant

- Mortgage payoff life insurance plan with a heart transplant

- Deceased spouse’s income replacement plan with a heart transplant

- Legacy insurance gift plan to family or loved ones with a heart transplant

- Medical or doctor bill life insurance plan with a heart transplant

We can help you with any of the plans above. Your pricing will depend on your age, health, and coverage amount for each program option.

How Can Funeral Funds Help Me?

Finding a policy with a heart transplant needn’t be frustrating; working with an independent final expense broker like Funeral Funds will make the process easier and quicker.

We will work with you every step to find the plan that fits your financial requirements and budget. You don’t have to waste your precious time searching for multiple insurance companies because we will do the dirty work for you.

We work with many A+ rated insurance carriers that specialize in covering high-risk clients like you. We will search all those companies to match you up with the best burial insurance company that gives the best rate.

We will assist you in securing the coverage you need at a rate you can afford. So, if you are looking for heart transplant funeral insurance, heart transplant burial insurance, or heart transplant life insurance, we can help. Fill out our quote form on this page or call us at (888) 862-9456, and we can give you an accurate quote.