2024 Burial Insurance for Hospice Patients [Use Caution]

last updated on July 22, 2024

last updated on July 22, 2024If you’re looking for burial insurance for hospice patients, you need to be aware that your burial, cremation, final expense, and life insurance options are limited.

!!! READ THIS FIRST !!!

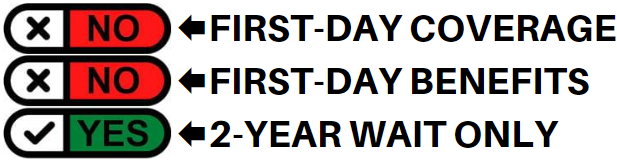

Being in hospice indicates a life-threatening health condition, and there are no insurance companies that offer 1st-day coverage to people in hospice.

We recommend people in hospice NOT purchase any life insurance product, as hospice patients will pass away before the mandatory 2-year waiting is completed.

In this post, We will explain who should buy guaranteed issue life insurance and why we don’t recommend guaranteed issue life insurance for hospice patients. We will even explain a few non-burial insurance options available to you.

FOR EASIER NAVIGATION:

- What Is My Best Insurance Option If I’m a Hospice Patient?

- Why We Don’t Recommend Guaranteed Issue Burial Insurance for Hospice Patients

- What Types of Burial Insurance Should I Avoid?

- What Type of Burial Insurance Is Best?

- If I’m a Hospice Patient, Do I Need a Medical Exam to Qualify for Burial Insurance?

- How Much Insurance Do I Need If I’m a Hospice Patient?

- How Should I Pay My Premiums?

- Hospice Patients and Burial Insurance Riders

- Who Should Buy Guaranteed Issue Life Insurance?

- Non-Burial Insurance Options for Hospice Patients

- When is the Best Time to Buy Burial Insurance?

- Benefits of Burial & Funeral Insurance

- Other Common Uses for Final Expense Life Insurance for Hospice Patients

- How Can Funeral Funds Help Me?

What Is My Best Insurance Option If I’m A Hospice Patient?

No insurance company will offer you first-day burial insurance coverage after being diagnosed with a short time to live.

If you are in hospice, your only option for insurance coverage is guaranteed issue life insurance. Guaranteed issue life insurance is available but has a 2-year waiting period, so this is also not a great plan for people entering hospice.

Best Option: Guaranteed issue burial insurance

Why We Don’t Recommend Guaranteed Issue Burial Insurance For Hospice Patients

The number one reason why we don’t recommend guaranteed issue life insurance for people in hospice is the two-year waiting period.

If your doctor thinks you’ll die in the next six months, buying guaranteed issue (GI) burial insurance will not help your family much.

GI policies only offer immediate first-day coverage for accidental death. There is also a mandatory two-year waiting period for any medical or health-related cause of death.

You must live for the first two years before your policy pays for a medical-related cause of death. This requirement makes guaranteed issue life insurance a terrible choice for people in hospice or people that are expected to die in the next 24 months.

This two-year waiting period is the insurance company’s way of not paying money to people who have procrastinated purchasing this insurance and are literally on their deathbed trying to buy burial insurance.

If you pass away during the waiting period for any reason other than an accident, your beneficiary will not receive the full death benefit. They will only receive the Return of Premium (ROP) plus interest, usually 5-10%.

If you die from an accident, the policy will pay your beneficiaries a 100% death benefit, even if you bought the policy recently.

What Types Of Burial Insurance Should I Avoid?

| PLANS TO AVOID | WHY? |

|---|---|

| Term life | Premiums increase after 5 years. Coverage ends after 80. |

| Pre-paid funeral plans | Expensive |

| Universal life | Tied with stocks |

| No health questions policies | With 2-year waiting period |

| Plans offering "teaser rates" | $9.95 per unit plans or $1 buys $100,000 coverage |

| Over priced plans | Insurance from TV and junk mail |

| Plans that accept mail-in payments | Risky |

| Plans that accept Direct Express | High lapse rate |

| Plans that accept Credit Cards | High lapse rate |

What Type Of Burial Insurance Is Best?

| FUNERAL FUNDS PLAN BENEFITS | INCLUDED |

|---|---|

| 1st Day Coverage | YES |

| Rates NEVER Increase | YES |

| Coverage NEVER Decreases | YES |

| Easy to get approved | YES |

| No Medical Exam | YES |

| Same Day Approval | YES |

| Death Claims Pay Fast | YES |

| Builds cash value | YES |

| Coverage Up To Age 121 | YES |

If I’m A Hospice Patient, Do I Need A Medical Exam To Qualify For Burial Insurance?

You are NOT required to take a medical exam to qualify for burial insurance for hospice patients.

When you apply for burial insurance, you only have to answer some basic questions about your health. The application process is simple; you don’t need to provide medical records or blood and urine samples.

You’ll get the official approval from the insurance company often within minutes!

How Much Insurance Do I Need If I’m A Hospice Patient?

The amount of burial insurance you should buy varies depending on your personal and financial circumstances. However, burial insurance should cover the cost of your funeral, burial, and final expenses.

The first step to figuring out how much burial insurance you need is to know your end-of-life expenses. Your funeral cost is often the biggest single expense you need to pay. Other end-of-life expenses to consider are your outstanding medical bills, living expenses, credit card bills, and other debts.

Here’s an example of a funeral cost breakdown from the National Funeral Directors Association.

| AVERAGE FUNERAL COST WITH VIEWING AND BURIAL | |

|---|---|

| Non-declinable basic services | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Hearse | $325 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Metal casket | $2,500 |

| Vault | $1,572 |

| Median Cost of a Funeral With Viewing and Burial | $9,420 |

| AVERAGE FUNERAL COST WITH VIEWING AND CREMATION | |

|---|---|

| Non-declinable basic services fee | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Cremation fee (if firm uses a third-party crematory) | $368 |

| Cremation Casket | $1,310 |

| Urn | $295 |

| Median Cost of a Funeral with Viewing and Cremation | $6,970 |

| Rental Casket | $995 |

| Alternate Cremation Container | $150 |

How Should I Pay My Premiums?

The best way to pay your premium is through a savings or checking account. We recommend you set a bank draft from your savings or checking account. That way, the bank will automatically pay your premium each month, and you don’t need to worry about your policy lapsing due to non-payment.

Hospice Patients And Burial Insurance Riders

Insurance policy riders add benefits to your policy. Adding insurance riders will enhance your policy to fit your needs. Some riders are built into your policy, while others can be added at an additional cost. Most riders are affordable, and it involves little to no underwriting.

Here’s a list of common burial insurance riders:

| FUNERAL FUNDS ADD-ONS | AVAILABILITY |

|---|---|

| Terminal Illness Add-On Benefit | Included with most plans |

| Nursing Home Care Add-On Benefit | Included with most plans |

Who Should Buy Guaranteed Issue Life Insurance?

We only sell guaranteed issue life insurance under these circumstances:

- They are not in hospice, or been advised to enter hospice

- The applicant has a life expectancy of two years or longer.

- The applicant has medical conditions that make them uninsurable for traditional life insurance.

- When the guaranteed issue is the most affordable policy because of their health.

- When applicants insist on no health questions asked life insurance application.

Guaranteed issue life insurance can provide essential insurance coverage to some people who need insurance but don’t have other options, but it is not appropriate if you are a hospice patient.

If you have any of these conditions, buying guaranteed issue burial insurance is often your best option:

These medical conditions are considered high-risk because they generally reduce the amount of time you will live. Applicants with any of these conditions will get declined if they have been diagnosed or treated for these conditions in the last two years.

- COPD with 24 hours a day oxygen use

- A heart attack, heart surgery, or stroke in the last 24 months

- Renal failure, on dialysis because of end-stage kidney disease

- Cancer diagnosis or treatment in the last 24 months

- Organ or tissue transplant

- Alzheimer’s disease

- AIDS

- Amputation due to disease

- Wheelchair use because of chronic illness

- Needing help with activities of daily living (eating, bathing, dressing, toileting, transferring, and continence)

- Confined in nursing facility

If you have any of these medical conditions, then guaranteed issue life insurance is your best option. Guaranteed issue burial insurance doesn’t ask health questions, so you will be approved for coverage even with these high-risk conditions.

Guaranteed issue life insurance should be your last option and is inappropriate for hospice patients.

Non-burial Insurance Options For Hospice Patients

If you are in hospice care and cannot qualify for life insurance, here are your non-burial insurance options:

1. Prepaid Funeral Plan

You have the option to take care of your funeral arrangements in advance. Instead of buying burial insurance, you can buy a prepaid funeral plan to cover your funeral and burial expenses.

You can buy a prepaid funeral plan at your nearest funeral home. Be warned, though. The final expenses are not cheap. Be prepared to pay between $8,000 and $15,000 to cover your final expenses.

If you choose this option, you need to immediately come up with the money because you must pay it in full.

2. Savings Accounts

Since you cannot qualify for burial insurance, you can open a savings account or joint savings account to deposit money to take care of your funeral and final expenses.

If you choose this option, you need to deposit around $8,000 to $15,000 in your account so it could be enough to cover your final expenses.

When you pass away, your loved ones can immediately access the funds in your savings account to pay for all the expenses associated with your death.

3. Totten Trust (Payable on Death Account)

If you don’t have burial insurance, you can opt to open a Payable On Death (POD) account. POD allows you to name a beneficiary on your bank account. Your beneficiary can access the funds on your account upon your death to pay for your final expenses.

This option is a bit harder, especially for fixed or limited income.

When Is The Best Time To Buy Burial Insurance?

You should buy burial insurance just before you become a hospice patient.

Waiting to buy burial insurance when you are in hospice is what procrastinators and poor planners do. Everyone knows they will die someday, so don’t wait until it’s too late to buy your burial, cremation, or final expense life insurance.

The best time to buy burial insurance is NOW! The younger you are, the lower your rates will be.

The healthier you are, the lower your rates will be.

Benefits Of Burial & Funeral Insurance

Here are some of the benefits of purchasing a burial or funeral policy:

- No medical exam or doctor’s visit is required – easy to get approved.

- Ease of issue – easy to qualify and get insurance coverage.

- No Money Down to get approved – have your policy start whenever you want.

- Level premium – your premium will never increase.

- Fixed death benefit – your death benefit will never decrease for any reason.

- Permanent protection – your policy can not be canceled by the life insurance company if you continue to pay your premiums.

- Tax-free – the death benefit is directly paid to your beneficiary tax-free upon your death.

- Cash value builds up – burial insurance is a whole life policy that builds cash value over time.

Other Common Uses For Final Expense Life Insurance For Hospice Patients

All of these examples are appropriate uses for Final Expense Life Insurance:

- Burial insurance plan for hospice patients

- Cremation insurance plan for hospice patients

- Funeral home insurance plan for hospice patients

- Final Expense insurance plan for hospice patients

- Prepaid funeral plan insurance for hospice patients

- Mortgage payment protection plan for hospice patients

- Mortgage payoff life insurance plan for hospice patients

- Deceased spouse’s income replacement plan for hospice patients

- Legacy insurance gift plan to family or loved ones for hospice patients

- Medical or doctor bill life insurance plan for hospice patients

We can help you with any of the plans above. Your pricing will depend on your age, health, and coverage amount for each program option.

How Can Funeral Funds Help Me?

Burial insurance should be purchased from an independent insurance agency like Funeral Funds. My agents and I can sell you burial insurance from over 30 insurance companies and pick the ones with the best plan at the best rate.

Save yourself the work of calling multiple insurance companies by working with us. We are paid a commission by the insurance company no matter what type of burial insurance you choose, and it won’t affect your pricing.

Answer the quote form on this page, and we will provide you with an accurate quote. Then, we will show you the plan with the most benefits at the lowest price.

6 Comments

Laura harris

Looking for creamation

Funeral Funds

https://funeralfunds.com/free-quote/

Willie E McGlothlin

looking for burial insurance for my dad

Funeral Funds

Visit this page for quotes – https://funeralfunds.com/free-quote/

ROBERT DEPPNER

How do apply for burial insurance for my husband?

d.o.b. 9/27/1940

served with the Marines for 4yrs.

Any information would be appreciated.

We are planning on cremation

Funeral Funds

Visit this page for quotes – https://funeralfunds.com/free-quote/