2024 Burial Insurance With Pre-existing Condition

last updated on July 22, 2024

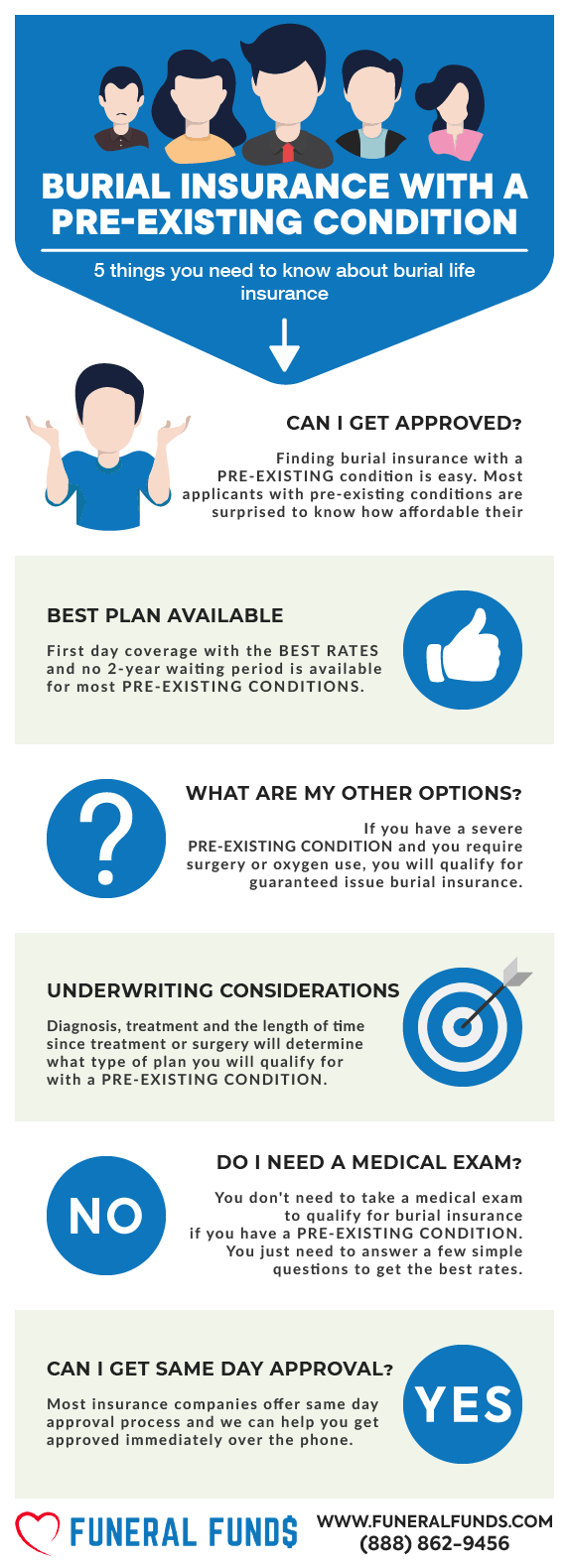

last updated on July 22, 2024Finding burial insurance with a pre-existing condition is possible. In fact, the majority of all health conditions we get as we get older are accepted by most life insurance companies.

Regardless of your pre-existing medical conditions or poor health, life insurance options are open for you.

This article is your comprehensive guide to burial insurance with a pre-existing condition. Click on the link to read more about each medical condition and how you can find affordable insurance coverage.

FOR EASIER NAVIGATION:

- What Is My Best Insurance Option If I Have a Pre-existing Condition?

- What Is a Pre-existing Medical Condition?

- What Types of Burial Insurance Should I Avoid?

- What Type of Burial Insurance Is Best?

- If I Have a Pre-existing Condition, Do I Need a Medical Exam to Qualify for Burial Insurance?

- Burial Insurance Underwriting If You Have a Pre-existing Condition

- How Much Insurance Do I Need If I Have a Pre-existing Condition?

- How Should I Pay My Premiums?

- Pre-existing Condition and Burial Insurance Riders

- Benefits of Burial & Funeral Insurance

- Other Common Uses for Final Expense Life Insurance with pre-existing condition

- What If I Have Been Declined Because Of My Pre-existing Condition?

- How Can Funeral Funds Help Me?

- Additional Questions & Answers On Burial Insurance With Pre-existing Condition

What Is My Best Insurance Option If I Have A Pre-existing Condition?

MOST COMMON PRE-EXISTING CONDITIONS

Most pre-existing conditions will qualify for level death benefit with a first-day coverage.

With first-day coverage, you will be covered from day one, and your beneficiaries will receive the full death benefit if you die for any reason.

Best Option: Level death benefit plan with first-day coverage

MORE SIGNIFICANT PRE-EXISTING CONDITIONS

If you have a more serious pre-existing condition, you will have other coverage options

Depending on the health condition, you may not qualify for a first-day coverage plan if you have:

- Terminal illness (your life expectancy is 24 months or less)

- You have cancer within the last 24 months

- End-stage kidney disease requiring dialysis

- Diagnosed with AIDS or HIV

- Alzheimer’s or dementia

- Congestive heart failure (CHF)

- Heart attack within the previous 12 months

- A circulatory surgery within the previous 12 months

- Full blown stroke (TIA mini-strokes do not count) within the previous 12 months

- Diabetic coma or insulin shock within the last 24 months

- Amputation due to diabetes

- Angina (chest pain) within the last 12 months

- Had a heart surgery within the previous 12 months

- Been recommended to have or had an organ transplant

- Oxygen use (only OK for sleep apnea)

- Currently in the hospital, skilled nursing facility, or hospice care

- Confined to a wheelchair or bed because of chronic illness

- Needing assistance with any activities of daily living such as eating, bathing, dressing, transferring and continence

If you have any of the pre-existing conditions above, you will only qualify for guaranteed issue burial insurance.

You are not required to take a medical exam or answer any health questions to qualify. You will be approved for coverage regardless of your pre-existing medical condition.

Additionally, guaranteed issue policies have a two-year waiting period where your beneficiary will not receive the full death benefit payout if you pass away from natural causes during this period. However, you will be fully covered for accidental death.

If you die from a natural cause such as a consequence of an illness during the two-year waiting period, your beneficiary will only receive all the premiums you paid into the policy plus 7-10% interest, depending on the insurance company.

Best Option: Guaranteed issue whole life insurance

What Is A Pre-existing Medical Condition?

A pre-existing medical condition is a health problem that is present before you apply for a policy. There are different policies available for people with certain health or medical conditions.

A pre-existing medical condition can take many forms.

Your condition can be treatable, or it could be terminal. Your condition could be with you since birth, or you may just be recently diagnosed.

A wide range of health issues can be considered a pre-existing medical condition, and it can either increase your premium or cause you not to qualify for coverage.

Below you will find different pre-existing conditions listed in alphabetical order. Click on the link to better understand your insurance options.

- Abdominal Aortic Aneurysm

- AIDS Acquired Immunodeficiency Syndrome

- ALS – Lou Gehrig’s Disease

- Alzheimer’s Disease

- Aneurysm

- Angina

- Angioplasty

- Arrhythmia

- Asthma

- Atrial Fibrillation

- Bipolar

- Brain Tumor

- Cancer

- Cerebral Palsy

- Cholesterol

- Chronic bronchitis

- Cirrhosis

- Congestive heart failure

- COPD – Chronic Obstructive Pulmonary Disease

- Coronary artery disease

- Defibrillator

- Dementia

- Diabetes

- Diabetic amputation

- Diabetic coma

- Dialysis

- Disability

- Down syndrome

- Emphysema

- Epilepsy

- Fibromyalgia

- Heart attack

- Heart bypass

- Heart Infection – Endocarditis

- Heart Murmur

- Heart transplant

- Heart valve surgery

- Hepatitis B

- High blood pressure

- HIV Human Immunodeficiency Virus

- Hodgkin’s Disease

- Huntington’s Disease

- Insulin shock

- Insulin use

- Kidney Disease/ Failure

- Leukemia

- Liver Disease

- Lung disease

- Lupus

- Melanoma

- Multiple sclerosis

- Muscular dystrophy

- Nephropathy

- Neuropathy

- Organ Transplant

- Oxygen

- Pacemaker

- Paralysis

- Parkinson’ Disease

- PTSD – Post-traumatic Stress Disorder

- PVD Peripheral Vascular Disease

- Schizophrenia

- Scleroderma

- Seizure

- Sickle Cell

- Sleep Apnea

- Stent

- Stroke

- Terminal Illness

- TIA Mini-stroke

- Valvular heart disease

If you have a pre-existing condition and want to purchase a new insurance policy, it’s important to know what types of plans you will qualify for and what your pricing will be.

What Types Of Burial Insurance Should I Avoid?

| PLANS TO AVOID | WHY? |

|---|---|

| Term life | Premiums increase after 5 years. Coverage ends after 80. |

| Pre-paid funeral plans | Expensive |

| Universal life | Tied with stocks |

| No health questions policies | With 2-year waiting period |

| Plans offering "teaser rates" | $9.95 per unit plans or $1 buys $100,000 coverage |

| Over priced plans | Insurance from TV and junk mail |

| Plans that accept mail-in payments | Risky |

| Plans that accept Direct Express | High lapse rate |

| Plans that accept Credit Cards | High lapse rate |

What Type Of Burial Insurance Is Best?

| FUNERAL FUNDS PLAN BENEFITS | INCLUDED |

|---|---|

| 1st Day Coverage | YES |

| Rates NEVER Increase | YES |

| Coverage NEVER Decreases | YES |

| Easy to get approved | YES |

| No Medical Exam | YES |

| Same Day Approval | YES |

| Death Claims Pay Fast | YES |

| Builds cash value | YES |

| Coverage Up To Age 121 | YES |

If I Have A Pre-existing Condition, Do I Need A Medical Exam To Qualify For Burial Insurance?

You are NOT required to take a medical exam to qualify for burial insurance with pre-existing conditions.

When you apply for burial insurance, you only have to answer some basic questions about your health. The application process is simple; you don’t need to provide medical records or blood and urine samples.

You’ll get the official approval from the insurance company often within minutes!

Burial Insurance Underwriting If You Have A Pre-existing Condition

Every life insurance company will assess your health to determine your level of risk.

Burial insurance companies have two ways of underwriting:

FIRST – They may ask you a series of health questions. Your answers to their questions will determine your eligibility.

SECOND – They will electronically review your prescription history to verify your health.

ANSWERS TO HEALTH QUESTIONS

When you want to apply for burial insurance with a pre-existing condition, your answers to the health questions will determine what plans you will qualify for and how much your premium will be.

Expect to see these health questions on the burial insurance application:

- Are you currently hospitalized, in a nursing facility, confined to a bed, or receiving hospice care?

- Do you have a terminal illness like cancer that may cause you to die within 24 months?

- Are you currently using oxygen for any lung or respiratory disorders?

- Have you been diagnosed or been treated for HIV or AIDS?

- Do you need help with activities of daily living like eating, bathing, dressing, toileting, transferring, or continence?

- Within the last 24 months, have you been diagnosed or treated by a doctor or had surgery for any of the following: health attack, heart blockage, heart valve disorder, stroke, or transient ischemic attack?

Different companies use different wording on their questions. They also have a different look-back period to medical conditions.

For example, you have high cholesterol or high blood pressure. You will never see any burial insurance companies ask about either of them. They don’t ask about high cholesterol or high blood pressure because they will still approve you for their best rates and first-day coverage with either of these health conditions.

Suppose you have a more serious medical condition like cancer. In that case, some insurance companies may ask if you have a diagnosis or cancer treatment in the previous four years, while others will ask if you’ve been diagnosed with cancer in the past two years only. If you have a history of cancer, look for a company offering burial insurance for cancer patients with a shorter look-back period.

It is important to note that if a burial insurance company does not ask about a specific pre-existing condition, it means they are accepting of it and will approve you for first-day coverage. The same principle applies to any other health issue.

PRESCRIPTION HISTORY CHECK

Every final expense company will perform a prescription history check. They will look at all the prescription medications you’ve been taking in the past few years.

They do this to verify your answers to the health questionnaire. If you say NO to the diabetes question, but the insurance company sees that you are taking Metformin, they will know you are not honest.

Every medication you take gives the company a better understanding of any underlying medical conditions. If they see a prescription, they will assume you are taking meds to treat the condition it is intended to cure.

Even if you answer no to the health question if you’re taking drugs for it, they will expect you to have pre-existing health or medical conditions.

Every insurance company has a different set of prescription medications they will or won’t accept. One company may deny you coverage for taking Heparin (a blood thinner), while another will accept your application.

HOW LIFE INSURANCE COMPANIES VIEW PRE-EXISTING MEDICAL CONDITIONS

Insurance companies will assess your medical condition according to your pre-existing condition’s seriousness and risk of dying prematurely. The worse your health is, the less likely the insurance company will offer you the lowest-priced life insurance coverage.

The type of plan you will qualify, for and your insurance premium will be based on your level of risk.

While some companies would deny you coverage because of your medical or health condition, some companies may have more experience with high-risk health conditions, and they will offer affordable protection.

How Much Insurance Do I Need If I Have A Pre-existing Condition?

The amount of burial insurance you should buy varies depending on your personal and financial circumstances. However, burial insurance should cover the cost of your funeral, burial, and final expenses.

The first step to figuring out how much burial insurance you need is to know your end-of-life expenses. Your funeral cost is often the biggest single expense you need to pay. Other end-of-life expenses to consider are your outstanding medical bills, living expenses, credit card bills, and other debts.

Here’s an example of a funeral cost breakdown from the National Funeral Directors Association.

| AVERAGE FUNERAL COST WITH VIEWING AND BURIAL | |

|---|---|

| Non-declinable basic services | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Hearse | $325 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Metal casket | $2,500 |

| Vault | $1,572 |

| Median Cost of a Funeral With Viewing and Burial | $9,420 |

| AVERAGE FUNERAL COST WITH VIEWING AND CREMATION | |

|---|---|

| Non-declinable basic services fee | $2,300 |

| Removal/ transfer of remains to funeral home | $350 |

| Embalming & preparation of the body | $1,050 |

| Use of facilities for viewing & funeral ceremony | $965 |

| Service car/van | $150 |

| Basic memorial printed package | $183 |

| Cremation fee (if firm uses a third-party crematory) | $368 |

| Cremation Casket | $1,310 |

| Urn | $295 |

| Median Cost of a Funeral with Viewing and Cremation | $6,970 |

| Rental Casket | $995 |

| Alternate Cremation Container | $150 |

How Should I Pay My Premiums?

The best way to pay your premium is through a savings or checking account. We recommend you set a bank draft from your savings or checking account. That way, the bank will automatically pay your premium each month and you don’t need to worry about your policy lapsing due to non-payment.

Pre-existing Condition And Burial Insurance Riders

Insurance policy riders add benefits to your policy. Adding insurance riders will enhance your policy to fit your needs. Some riders are built into your policy, while other riders can be added at an additional cost. Most riders are affordable, and it involves little to no underwriting.

Here’s a list of common burial insurance riders:

| FUNERAL FUNDS ADD-ONS | AVAILABILITY |

|---|---|

| Terminal Illness Add-On Benefit | Included with most plans |

| Nursing Home Care Add-On Benefit | Included with most plans |

BENEFITS OF BURIAL & FUNERAL INSURANCE

Here are some of the benefits of purchasing a burial or funeral policy

- No medical exam or doctor’s visit is required – easy to get approved.

- Ease of issue – easy to qualify and get insurance coverage.

- No Money Down to get approved – have your policy start whenever you want.

- Level premium – your premium will never increase.

- Fixed death benefit – your death benefit will never decrease for any reason.

- Permanent protection – your policy can not be canceled by the life insurance company if you continue to pay your premiums.

- Tax-free – the death benefit is directly paid to your beneficiary tax-free upon your death.

- Cash value builds up – burial insurance is a whole life policy that builds cash value over time.

Other Common Uses For Final Expense Life Insurance With Pre-existing Condition

All of these examples are appropriate uses for Final Expense Life Insurance:

- Burial insurance plan with pre-existing condition

- Cremation insurance plan with pre-existing condition

- Funeral home insurance plan with pre-existing condition

- Final Expense insurance plan with pre-existing condition

- Prepaid funeral plan insurance with pre-existing condition

- Mortgage payment protection plan with pre-existing condition

- Mortgage payoff life insurance plan with pre-existing condition

- Deceased spouse’s income replacement plan with pre-existing condition

- Legacy insurance gift plan to family or loved ones with pre-existing condition

- Medical or doctor bill life insurance plan with pre-existing condition

We can help you with any of the plans above. Your pricing will depend on your age, health, and coverage amount for each program option.

What If I Have Been Declined Because Of My Pre-existing Condition?

If you have been declined for life insurance coverage, don’t give up hope.

All too often, the company you applied with is not the right company for you. We could help you get approved for life insurance coverage. We can shop your case at multiple life insurance companies to get the best plan for your needs.

If you are considered uninsurable because of your pre-existing condition, we can get you a guaranteed issue life insurance plan. This plan does not require a medical exam or health questions.

You will be approved for coverage regardless of your pre-existing medical condition.

How Can Funeral Funds Help Me?

Finding a policy if you have breast cancer needn’t be frustrating; working with an independent agency like Funeral Funds will make the process easier and quicker.

We will work with you every step to find the plan that fits your financial requirements and budget. You don’t have to waste your precious time searching for multiple insurance companies because we will do the work for you.

We work with many A+ rated insurance carriers that specialize in covering high-risk clients like you. We will search all those companies and match you up with the best burial insurance company that gives the best rate.

We will assist you in securing the coverage you need at a rate you can afford, so if you are looking for breast cancer funeral, breast cancer burial, or life insurance. Fill out our quote form on this page or call us at (888) 862-9456, and we can give you an accurate quote.

Additional Questions & Answers On Burial Insurance With Pre-existing Condition

What is meant by pre existing condition?

Pre-existing condition refers to any medical condition present before an individual’s policy went into effect. Most insurance policies do not cover costs related to pre-existing conditions, so it’s important to check with your insurer before you buy a policy. Some insurers will waive the pre-existing condition exclusion if you have been continuously covered by insurance for a certain period before enrolling in your new policy.

What is a pre-existing condition in insurance?

A pre-existing condition is any medical condition present before an individual’s policy is enacted. Most insurance policies do not cover costs related to pre-existing conditions, so it’s important to check with your insurer before you buy a policy.

What qualifies as a pre-existing condition?

There is no definitive list of pre-existing conditions, as the definition can vary from insurer to insurer. However, common examples of pre-existing conditions include cancer, heart disease, and diabetes.

I have a pre-existing condition. Can I still buy burial insurance?

Yes, you can still buy burial insurance even if you have a pre-existing condition. However, your options may be limited and the coverage you’re able to get may be less than what you would receive if you did not have a pre-existing condition. It’s important to compare policies from different insurers to see what’s available to you.

Can I be denied insurance because of a pre-existing condition?

Yes, you can be denied insurance because of a pre-existing condition. Most insurers will not cover costs related to pre-existing conditions, so it’s important to check with your insurer before you buy a policy.

Is it hard to get life insurance with pre-existing conditions?

It is not hard to get life insurance with pre-existing conditions. However, your options may be limited, and the coverage you can get may be less than what you would receive if you did not have a pre-existing condition. It’s important to compare policies from different insurers to see what’s available to you.

What is the difference between pre-existing conditions and exclusions?

Pre-existing condition refers to any medical condition present before an individual’s policy was enacted. Exclusions are specific conditions that are not covered by a policy. Most policies do not cover costs related to pre-existing conditions, so it’s important to check with your insurer before you buy a policy.

What is the difference between pre-existing conditions and preexisting conditions?

There is no difference between the two terms. Pre-existing condition refers to any medical condition that was present before an individual’s policy went into effect. Most insurance policies do not cover costs related to pre-existing conditions, so it’s important to check with your insurer before you buy a policy.

Is high blood pressure a pre-existing condition for life insurance?

High blood pressure, or hypertension, is a common pre-existing condition that can affect your eligibility for life insurance. If you have high blood pressure, you may still be able to get life insurance. Insurers will typically classify people with high blood pressure as being at an increased risk of developing health problems in the future.

What is pre-existing condition waiting period?

A pre-existing condition waiting period is the amount of time that must pass after you purchase a policy before your coverage will be active.

Is high cholesterol a pre-existing condition?

High cholesterol is a pre-existing condition that can affect your eligibility for some types of life insurance. If you have high cholesterol, you may still be able to get life insurance. Insurers will typically classify people with high cholesterol as being at an increased risk of developing health problems in the future.

I have a pre-existing condition. What should I do?

Some insurers will waive the pre-existing condition exclusion if you have been continuously covered by insurance for a certain period before enrolling in your new policy. You may also want to consider purchasing burial insurance, which typically does not have a pre-existing condition exclusion.

What is acute onset of pre-existing conditions?

Acute onset of pre-existing conditions is a term used in health insurance policies to describe a sudden, unexpected onset of a pre-existing condition. This can happen when you’re not expecting it and can result in high medical expenses. If you have an acute onset of a pre-existing condition, your insurer may be able to deny you coverage or charge you higher premiums.

Is back pain considered a pre-existing condition?

Back pain is a common pre-existing condition that can affect your eligibility for life insurance. If you have back pain, you may still be able to get life insurance. Insurers will want to understand what is causing the back pain before approving a policy.

What is the pre-existing condition exclusion period?

The pre-existing condition exclusion period is the amount of time an insurer will not cover any costs related to a pre-existing condition. This can be very costly for someone with a pre-existing condition, as they may have to pay out-of-pocket medical expenses.

Is cancer a pre-existing condition for life insurance?

Cancer is a pre-existing condition that can affect your eligibility for life insurance. If you have cancer, you may still be able to get life insurance. Insurers will typically classify cancer at an increased risk of developing health problems in the future.

What is a pre-existing condition for people with diabetes?

People with diabetes are considered to have a pre-existing condition. If you have diabetes, you may still be able to get life insurance. Insurers will typically classify people with diabetes as being at an increased risk of developing health problems in the future.

Is arthritis a pre-existing condition?

Arthritis is a pre-existing condition that can affect your eligibility for life insurance. If you have arthritis, you can still get life insurance.

Is heart disease a pre-existing condition?

Heart disease is a pre-existing condition that can affect your eligibility for life insurance. If you have heart disease, you may still be able to get life insurance. Insurers will typically classify people with heart disease as being at an increased risk of developing health problems in the future.

I have a pre-existing condition. Can I get final expense life insurance?

Some insurers will waive the pre-existing condition exclusion if you have been continuously covered by insurance for a certain period of time before enrolling in your new policy.

Is high blood pressure a heart condition for insurance?

High blood pressure is a heart condition that can affect your eligibility for life insurance. If you have high blood pressure, you may still be able to get life insurance. Insurers will typically classify people with high blood pressure as being at an increased risk of developing health problems in the future.

What is considered high cholesterol for life insurance?

In general, most insurers consider anything above 240mg/dL to be high cholesterol.

Will I be denied life insurance for high cholesterol?

Most insurers will not deny coverage to someone based on their high cholesterol. However, if you have a history of heart disease or other health problems related to high cholesterol, you may be considered to have a pre-existing condition and may be denied life insurance.

Can you get life insurance with high triglycerides?

Most insurers will not deny coverage to someone based on their high triglycerides. However, if you have a history of heart disease or other health problems related to high triglycerides, you may be considered to have a pre-existing condition and may be denied life insurance.

Is asthma a pre-existing condition?

Asthma is a pre-existing condition that can affect your eligibility for life insurance. If you have asthma, you may still be able to get life insurance. Insurers will typically classify people with asthma as potentially having an increased risk of developing health problems in the future.

Do I need to tell insurance about medical conditions?

Yes, you need to be honest with your insurance company and not lie on your application for coverage.

Can someone with Type 2 diabetes get life insurance?

Yes, people with Type 2 diabetes can often get life insurance. However, the insurer may have a stricter underwriting process.

Is acid reflux a pre-existing condition?

No insurers will deny coverage to someone based on their acid reflux. However, if you have a history of heart disease or other health problems related to acid reflux, you may be considered to have a pre-existing condition and may be denied life insurance.

Is a stroke considered a pre-existing condition?

A stroke is a pre-existing condition that can affect your eligibility for life insurance. If you have had a stroke, you may still be able to get life insurance. Insurers will typically classify people who have had a stroke as being at an increased risk of developing health problems in the future.

Is high blood sugar a pre-existing condition?

High blood sugar is a pre-existing condition that can affect your eligibility for life insurance. If you have high blood sugar, you may still be able to get life insurance. Insurers will typically classify people with high blood sugar as being at an increased risk of developing health problems in the future.

Can a diabetic buy cremation insurance?

Yes, diabetics can buy cremation insurance. Cremation insurance is a type of life insurance that pays for your cremation expenses in the event of your death. Cremation insurance policies do not typically have health questions or medical exams, so you can be approved for coverage regardless of your health status.

Can I get funeral insurance if I have cancer?

Cancer is a pre-existing condition that can affect your eligibility for funeral insurance. If you have cancer, you may still be able to get life insurance. Insurers will typically classify people with cancer as being at an increased risk of developing health problems in the future.

Why would I get turned down for life insurance?

There are many reasons why you may be denied life insurance. Some of the most common reasons include having a pre-existing condition, being overweight, or having a family history of health problems.

What is the waiting period for pre existing conditions?

The waiting period for pre-existing conditions varies from insurer to insurer. Some insurers have no waiting period, while others may have a waiting period of up to 24 months.